Looking to generate income in retirement?

Covered calls are a key component of our tried-and-true Snider Investment Method strategy. As covered call advisors, we use our extensive knowledge in investing to train and empower both novice and experienced investors to write covered calls and boost the income from their portfolios.

Watch the Covered Call Blueprint

RSVP for a Live Event

How Does the Snider Method Work?

Learn Our Comprehensive Strategy

Take our online or live workshop for retirement education and learn our complete portfolio management strategy focused on earning income with options.

Invest With Our Software

Our proprietary stock analysis and automated trading software, Lattco, guides you through the trading process each month.

Become a Confident Investor

The Snider Investment Method leaves no room for emotions or the common mistakes of the average investor.

Our simple, step-by-step retirement investment process leaves you feeling confident. Learn more by downloading our Snider Investment Method Owner’s Manual.

Would you like to generate more income from your portfolio?

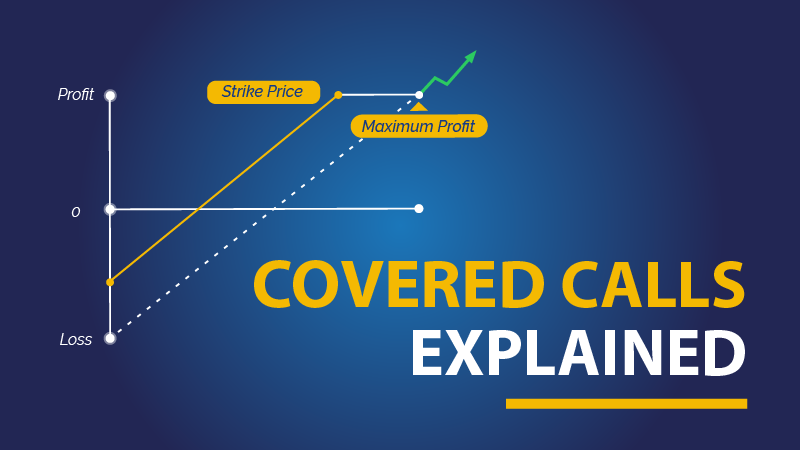

The Snider Investment Method uses covered calls as our primary tool to maximize the income from a stock portfolio. If you are unsure about options or new to covered calls, get started with What is a Covered Call? Learn the Pros and Cons

Already Trading Covered Calls? Check out our Free Covered Call Screener!

Learn to Invest from Trusted Covered Call Advisors

20 Years of Covered Call Experience

Smart financial planning decisions can boost your income, avoid costly mistakes, and make your money last longer. While simpler than most option strategies, writing covered calls requires a basic understanding of options and how they work. As covered call advisors, we can help you place your first trade or optimize your strategy.

Don’t Be Unprepared for Retirement

The Ultimate Planning Checklist for Retirement Education

A Perfect Cheat-Sheet to Enjoying Financial Security in Retirement

Too many people aren’t well prepared when they reach retirement – too much debt, too little invested, life-expectancy underestimated, stock markets too volatile. This simple CHECKLIST covers all the bases, giving you a clear snapshot of everything that needs to be done to get you ready for, not just any retirement, but an absolute dream retirement!

Retirement Checklist Instant Download

Social Security, Medicare, Investments: Where do you begin when it’s time to seriously consider retirement?

Worried about using up your retirement funds?

The Snider Investment Method provides simple and easy retirement education so you can earn a portfolio paycheck after you retire. Allowing you to worry less and actually enjoy retirement.

Start Your Retirement Education

Which retirement investment path is best for you?

Done For You

We do the work, you enjoy the results. Snider Advisors offers full-service portfolio management using our time-tested strategy, the Snider Investment Method.

Asset Management

Schedule a free consultation to help determine if the Snider Method is the right fit for your portfolio.

Get Started

Do It Yourself

Take the reins of your portfolio and execute your own trades. Eliminate the management fees, and always have a professional team by your side when you need help.

Learn Our Strategy

Read more about how our trading software and online course can get you and your portfolio back on the right track.

Learn More

October 17th at 12:00 PM CDT

Join us for a comprehensive look into the Snider Investment Method Learn More

COMING SOON

Join us at this live event to learn the principles behind the Snider Investment Method. Learn More

Fast Track Online Course

All the training, tools, and support you need to become a confident investor. Learn More