Liberty Street Economics2026-06-22T14:49:21Zhttps://libertystreeteconomics.newyorkfed.org/feed/atom/WordPress<![CDATA[The New York Fed DSGE Model Forecast—June 2026]]>https://libertystreeteconomics.newyorkfed.org/?p=433182026-06-22T14:49:21Z2026-06-22T13:00:00ZMarch 2026. To summarize, inflation forecasts are higher in 2026 than predicted in March. Projections for the short-run real natural rate of interest (r*) increased slightly relative to March.]]>

Marco Del Negro, Keshav Dogra, Elena Elbarmi, Donggyu Lee, and Michael Pham

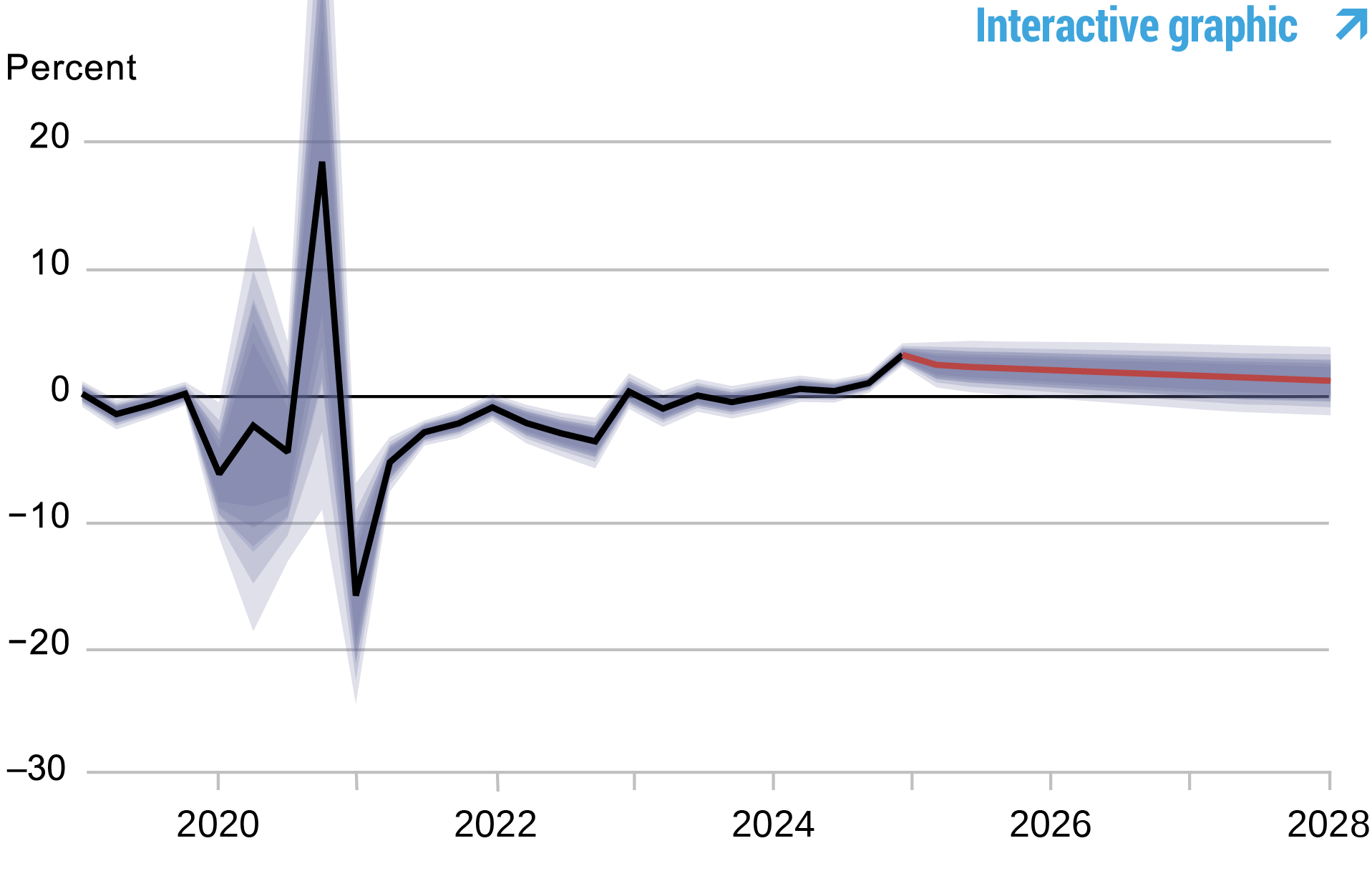

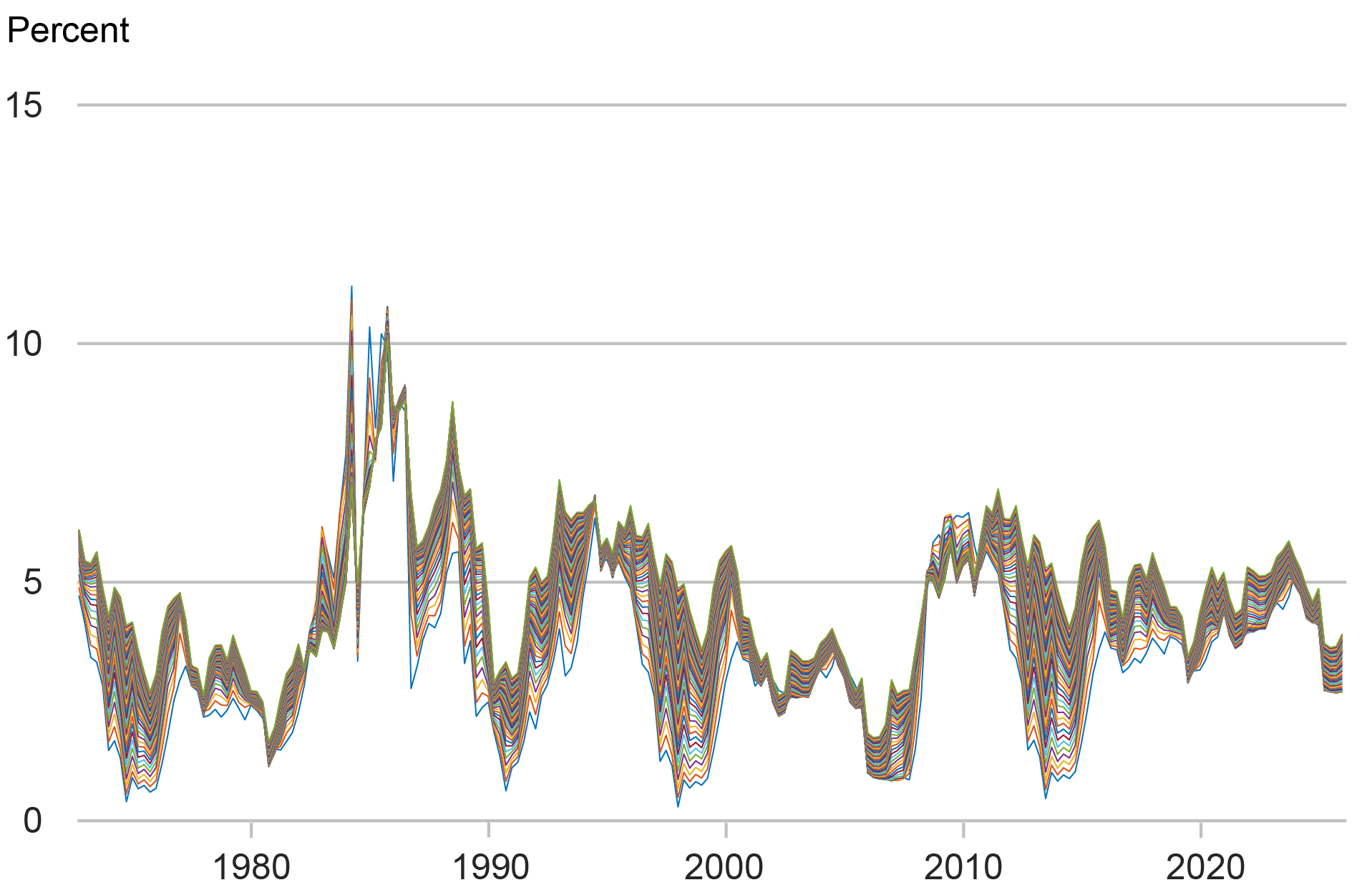

This post presents an update of the economic forecasts generated by the Federal Reserve Bank of New York’s dynamic stochastic general equilibrium (DSGE) model. We describe very briefly our forecast and its change since March 2026. To summarize, inflation forecasts are higher in 2026 than predicted in March. Projections for the short-run real natural rate of interest (r*) increased slightly relative to March.

Note: The DSGE model forecast is not an official New York Fed forecast, but only an input to the Research staff’s overall forecasting process. For more information about the model and variables discussed here, see our DSGE model Q & A.

The New York Fed DSGE model forecasts use data released through 2026:Q1, augmented for 2026:Q2 with median forecasts for real GDP growth and core PCE inflation from the May release of the Philadelphia Fed Survey of Professional Forecasters (SPF), as well as the yields on 10-year Treasury securities and Baa corporate bonds based on 2026:Q2 averages up to May 27. Starting in 2021:Q4, the expected federal funds rate (FFR) between one and six quarters into the future is restricted to equal the corresponding median point forecast from the latest available Survey of Market Expectations (SME) in the corresponding quarter. For the current projection, this is the April SME.

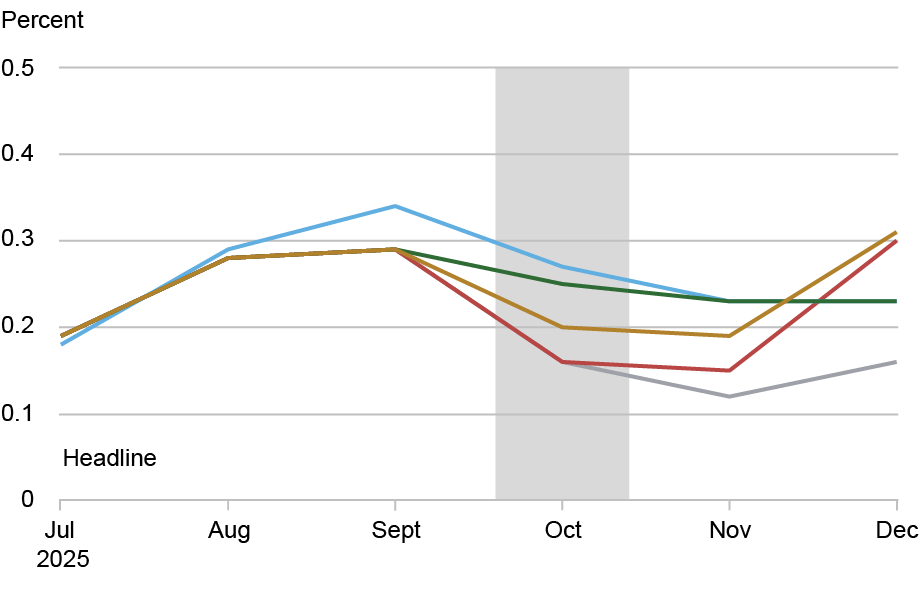

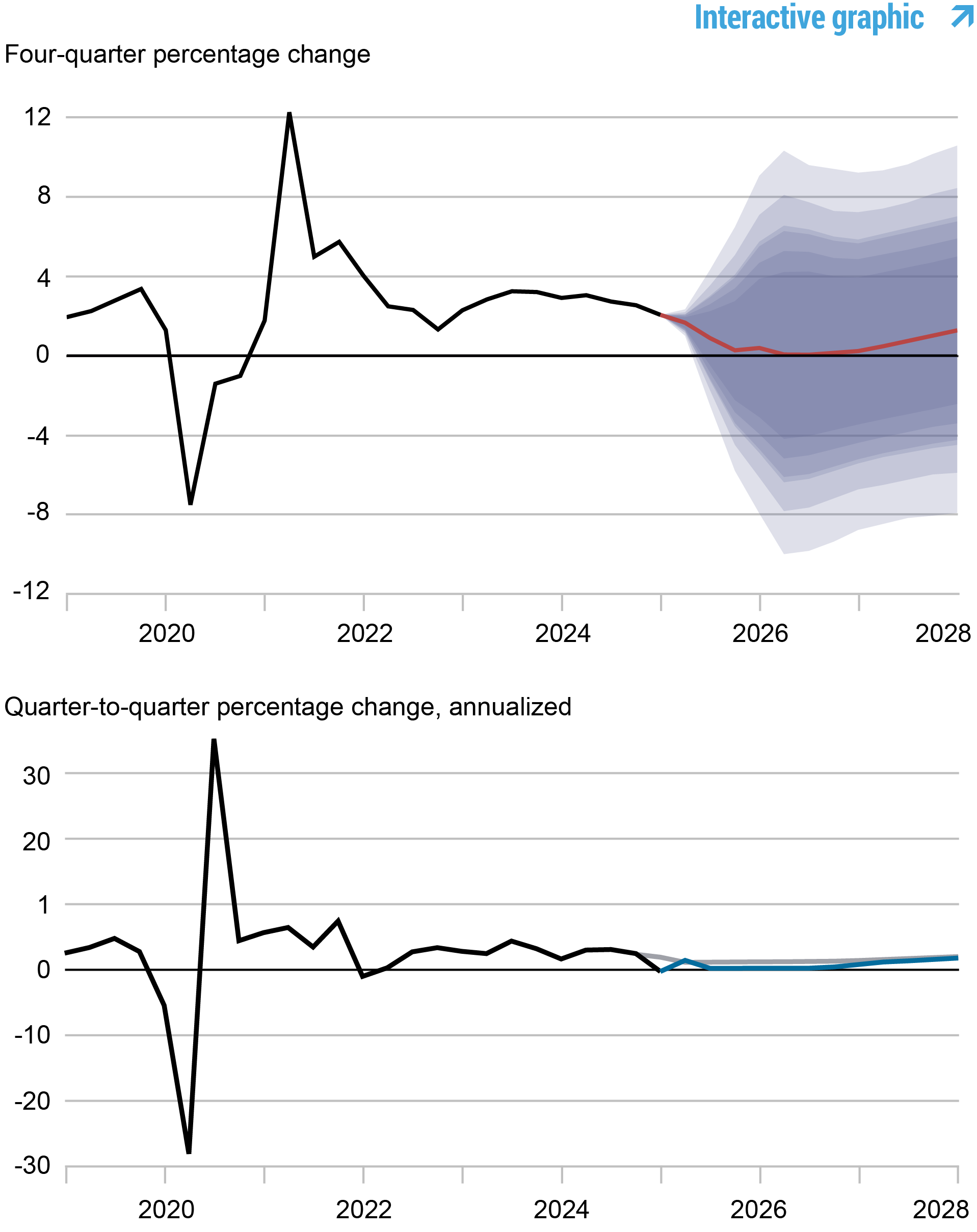

The SPF expects core inflation in 2026:Q2 to be more than 1 percent higher in annualized terms than the DSGE model expected in March. In light of this forecast miss (if the SPF turns out to be correct), the model revised its inflation forecasts upward in 2026, from 2.4 to 3.1 percent. The DSGE attributes the forecast error to mark-up shocks, which may capture the effects of both tariff and energy shocks. The model views the impact of these shocks as vanishing by the end of the year and hence the inflation forecasts are largely unchanged throughout the rest of the forecast horizon.

On the output front, the DSGE is more upbeat than it was in March, although its projections remain somewhat pessimistic. The model does see the positive growth effect of the AI-related boom in investment—positive MEI (marginal efficiency of investment) shocks push output up, especially in 2026—but also believes that the adverse markup shocks will push down growth in the future.

The model’s predictions for the short-run real natural rate of interest (r*) increased by 0.1 percentage point relative to March (2.0, 1.7, and 1.3 percent for 2026, 2027, and 2028, versus 1.9, 1.6, and 1.3 percent), partly reflecting higher total factor productivity (TFP).

Forecast Comparison

Forecast Period

2026

2027

2028

2029

Date of Forecast

Jun26

Mar26

Jun26

Mar26

Jun26

Mar26

Jun26

Mar26

GDP growth (Q4/Q4)

1.2 (-2.2, 4.5)

1.0 (-3.4, 5.6)

0.2 (-5.0, 5.2)

0.2 (-5.1, 5.4)

0.7 (-4.8, 6.0)

0.8 (-4.7, 6.3)

1.5 (-4.1, 6.9)

1.3 (-4.4, 6.9)

Core PCE inflation (Q4/Q4)

3.1 (2.5, 3.7)

2.5 (1.6, 3.3)

1.8 (0.7, 3.0)

2.0 (0.8, 3.2)

1.6 (0.4, 2.9)

1.9 (0.6, 3.2)

1.7 (0.4, 3.0)

2.0 (0.6, 3.3)

Real natural rate of interest (Q4)

2.0 (0.7, 3.3)

1.9 (0.6, 3.3)

1.7 (0.2, 3.1)

1.6 (0.0, 3.1)

1.3 (-0.3, 2.9)

1.2 (-0.4, 2.8)

1.1 (-0.5, 2.8)

1.0 (-0.6, 2.7)

Source: Authors’ calculations. Notes: This table lists the forecasts of output growth, core PCE inflation, and the real natural rate of interest from the June 2026 and March 2026 forecasts. The numbers outside parentheses are the mean forecasts, and the numbers in parentheses are the 68 percent bands.

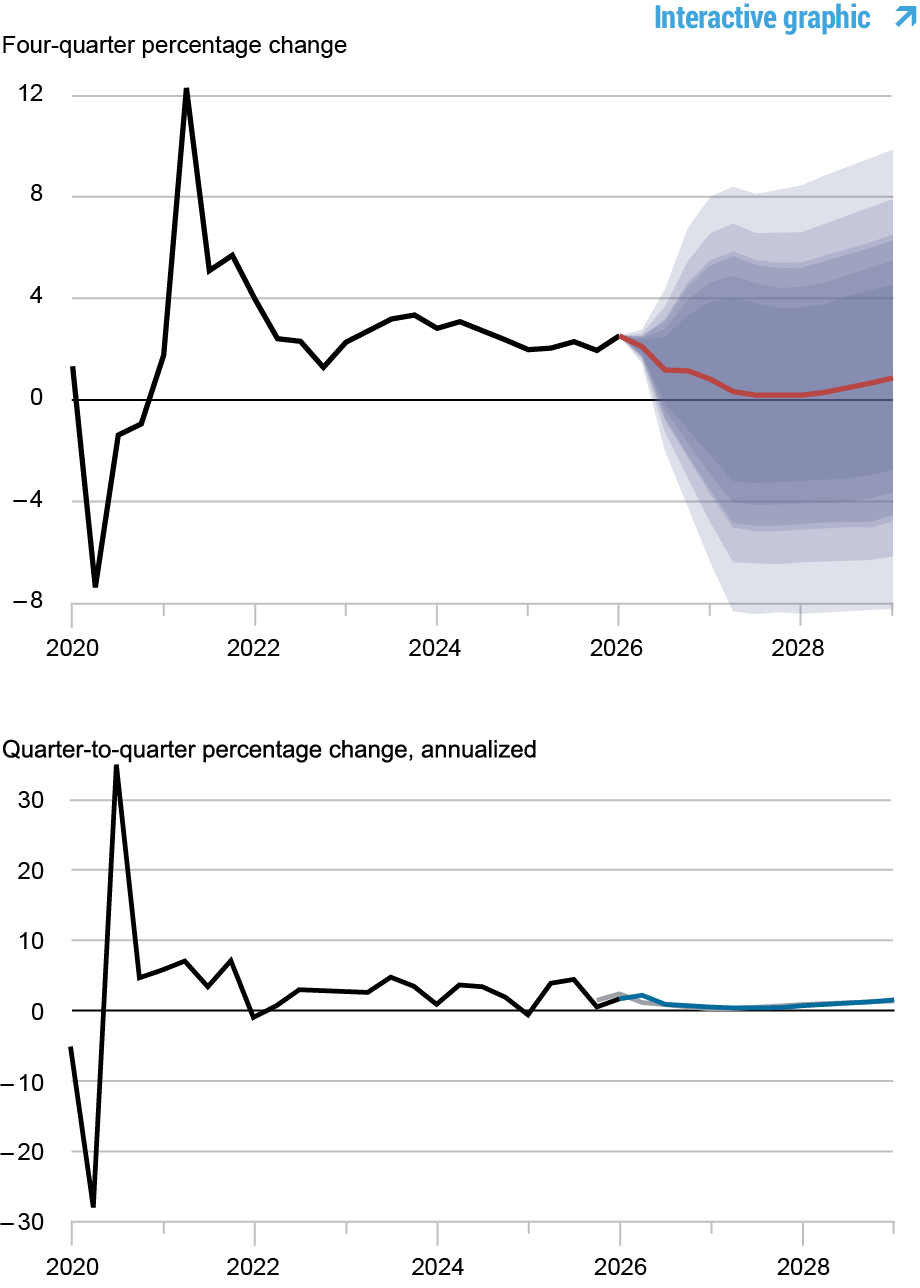

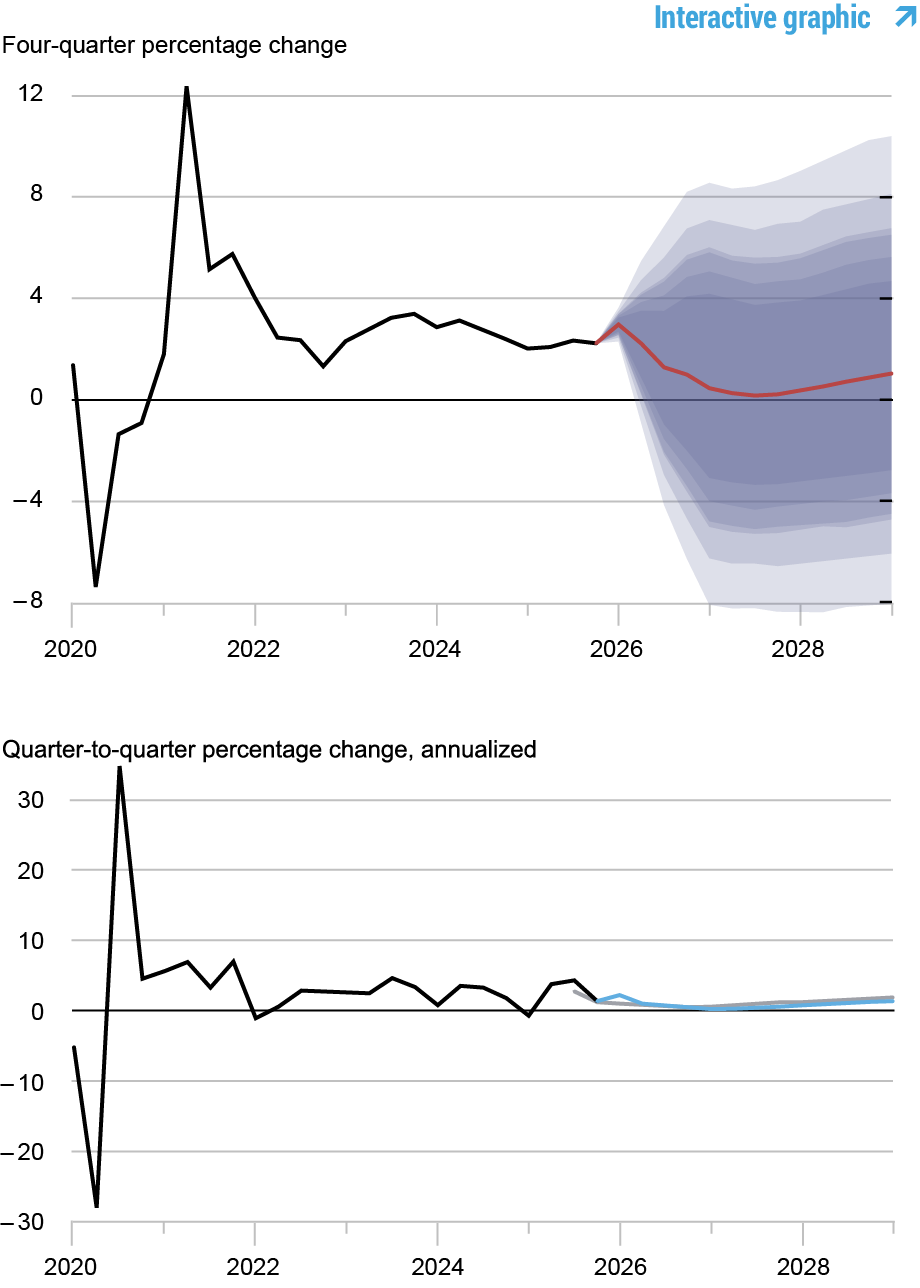

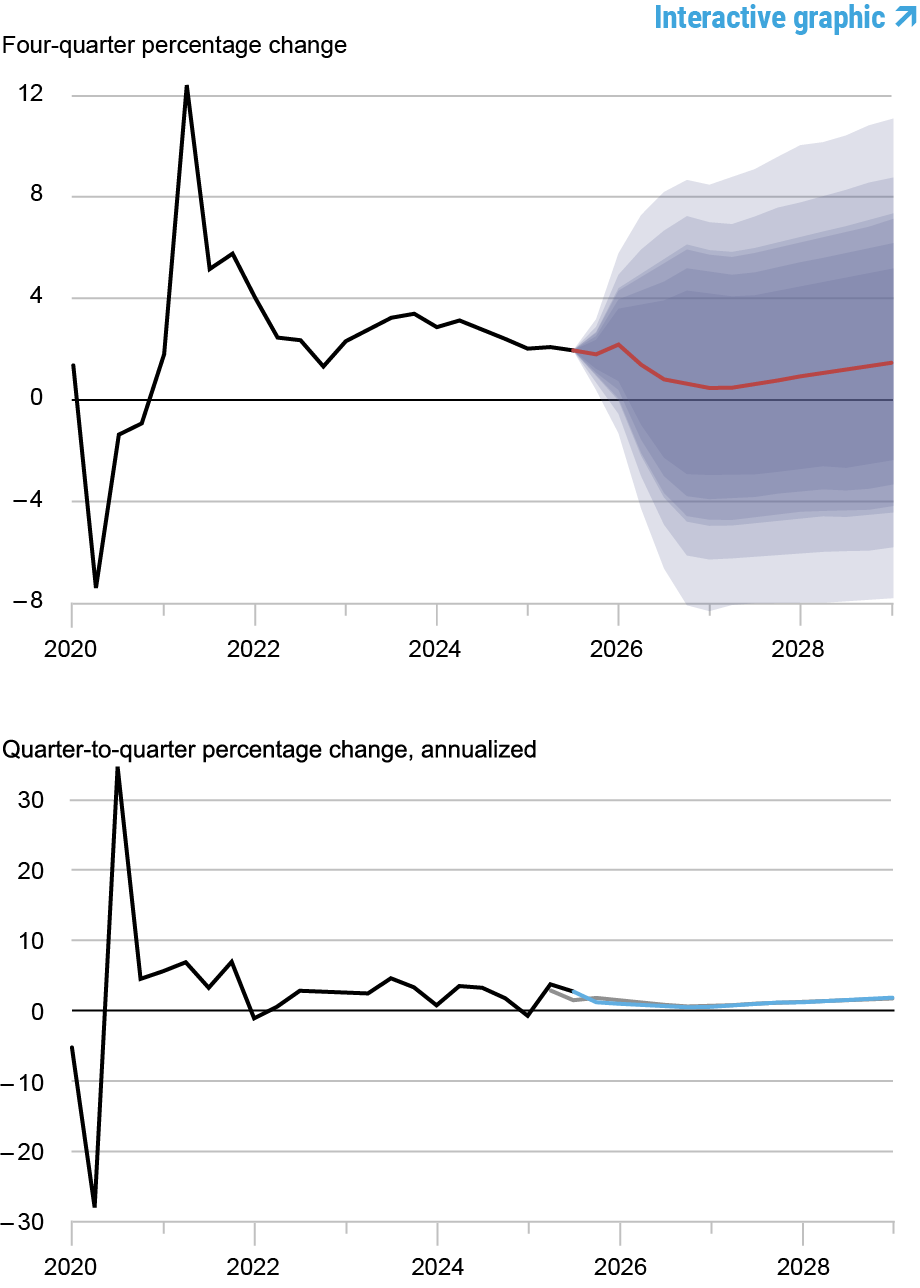

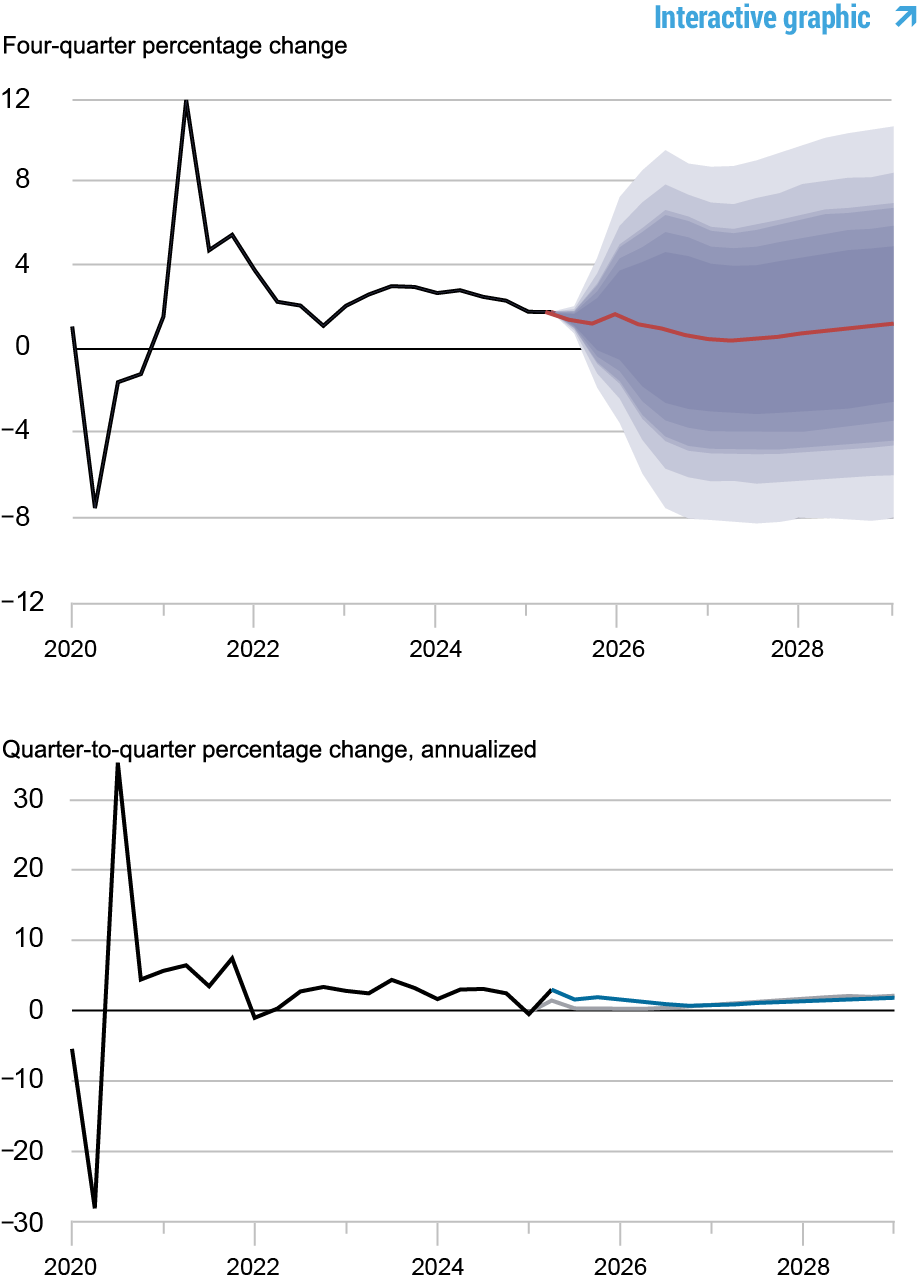

Forecasts of Output Growth

Source: Authors’ calculations. Notes: These two panels depict output growth. In the top panel, the black line indicates actual data and the red line shows the model forecasts. The shaded areas mark the uncertainty associated with our forecasts at 50, 60, 70, 80, and 90 percent probability intervals. In the bottom panel, the blue line shows the current forecast (quarter-to-quarter, annualized), and the gray line shows the March 2026 forecast.

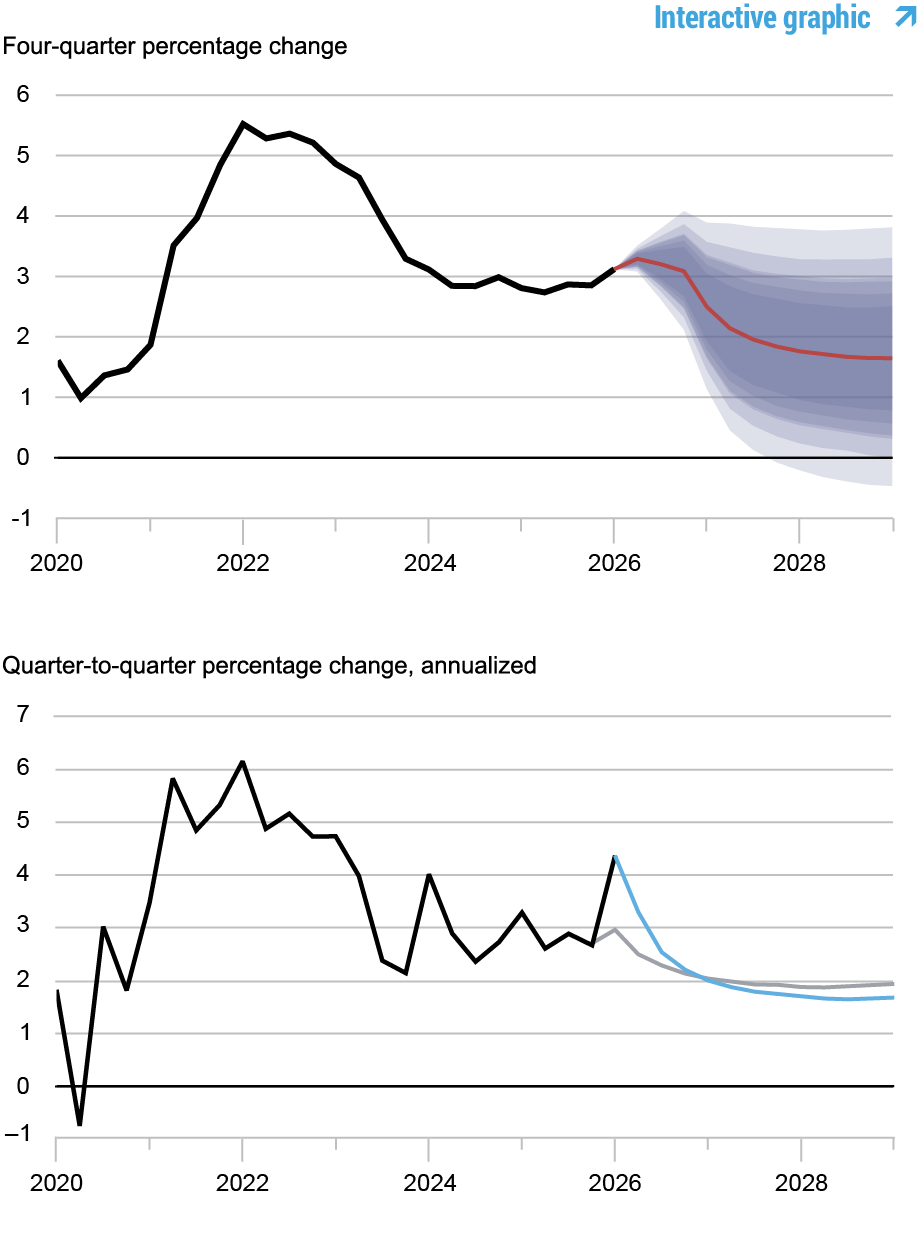

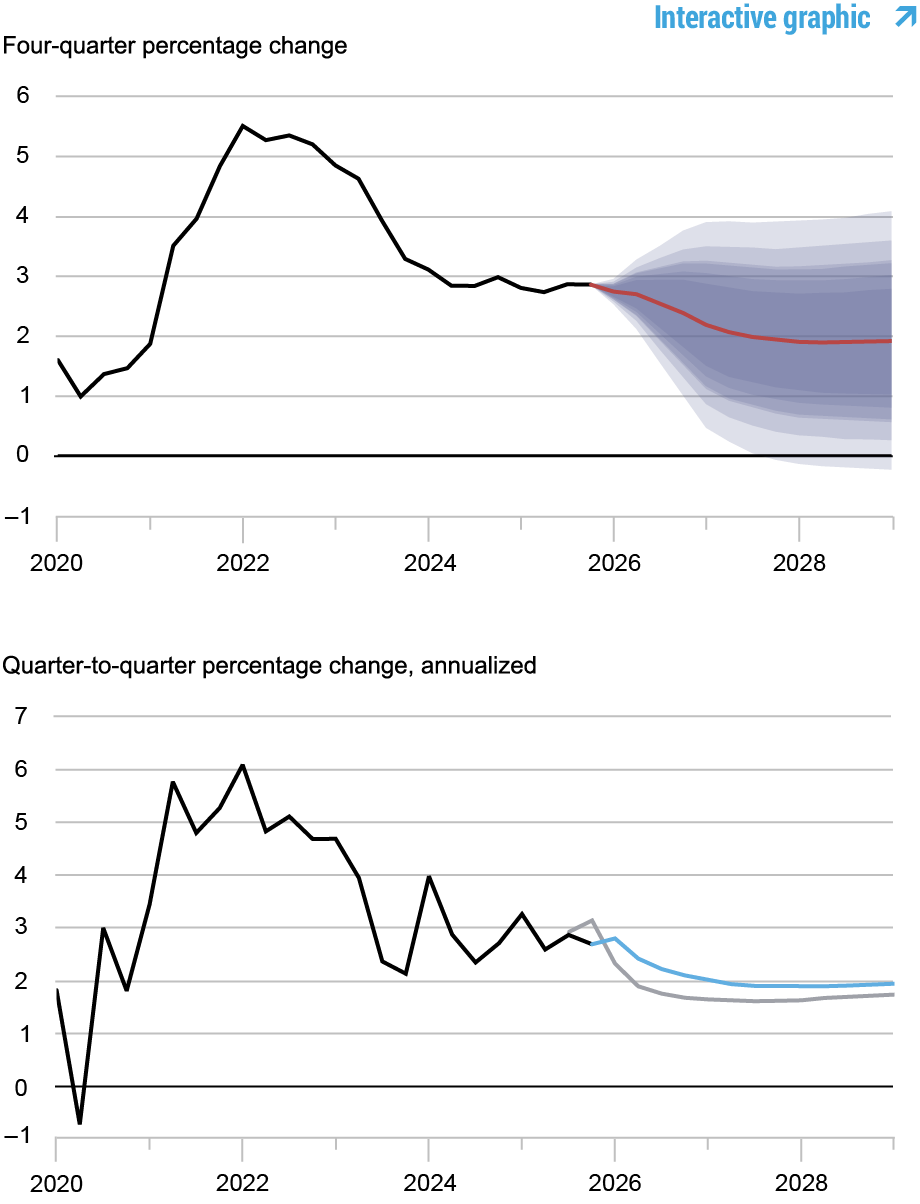

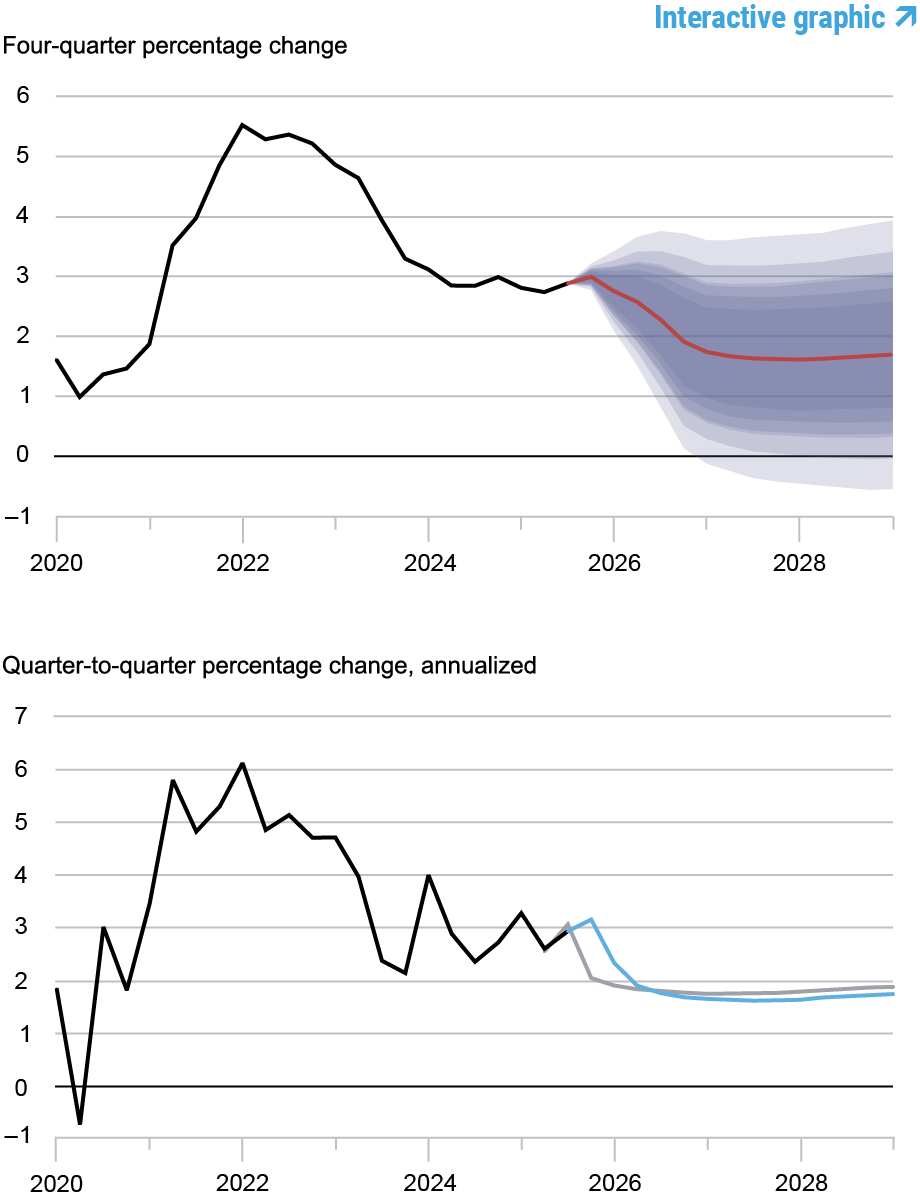

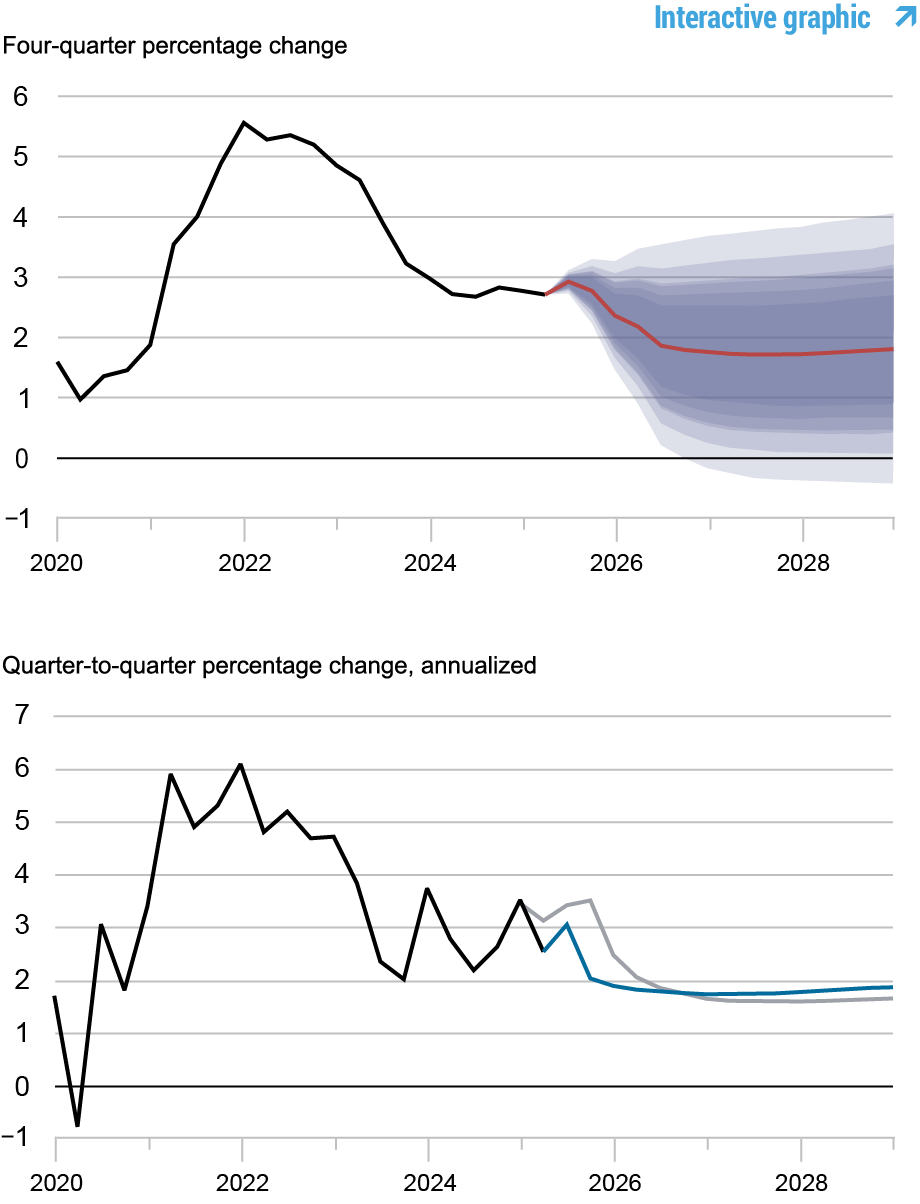

Forecasts of Inflation

Source: Authors’ calculations. Notes: These two panels depict core personal consumption expenditures (PCE) inflation. In the top panel, the black line indicates actual data and the red line shows the model forecasts. The shaded areas mark the uncertainty associated with our forecasts at 50, 60, 70, 80, and 90 percent probability intervals. In the bottom panel, the blue line shows the current forecast (quarter-to-quarter, annualized), and the gray line shows the March 2026 forecast.

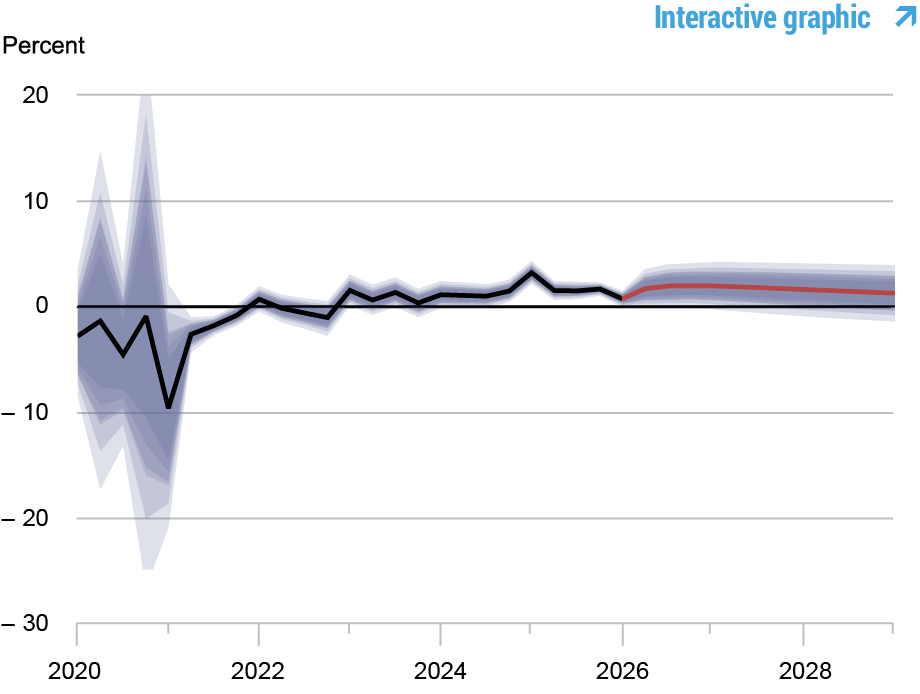

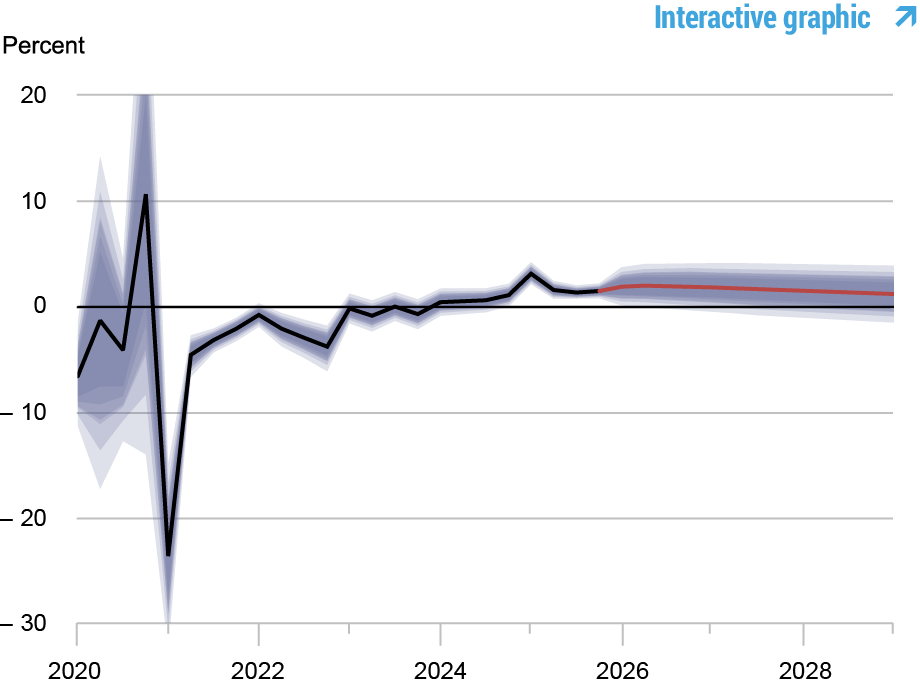

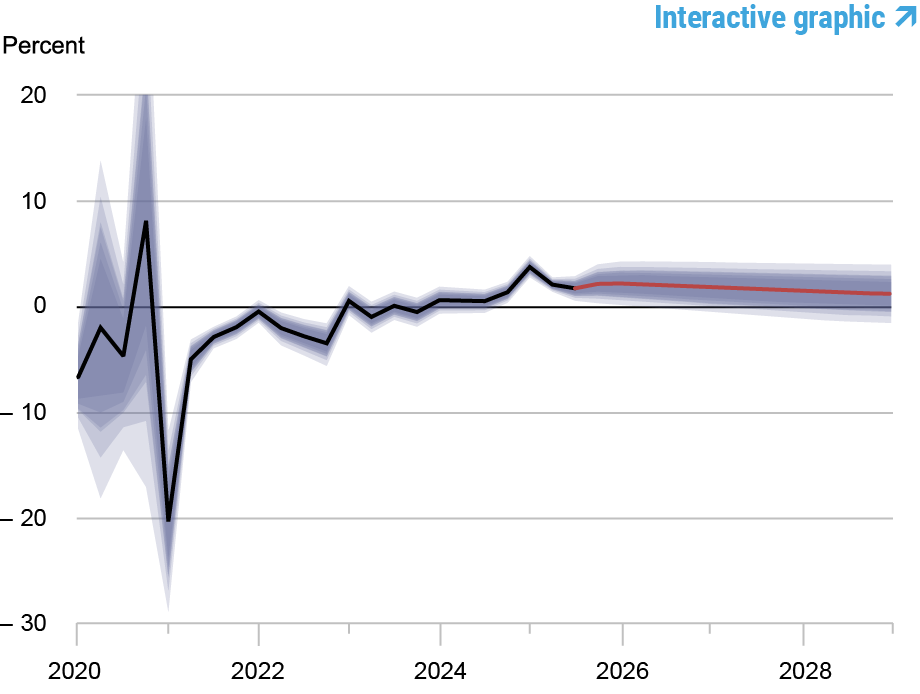

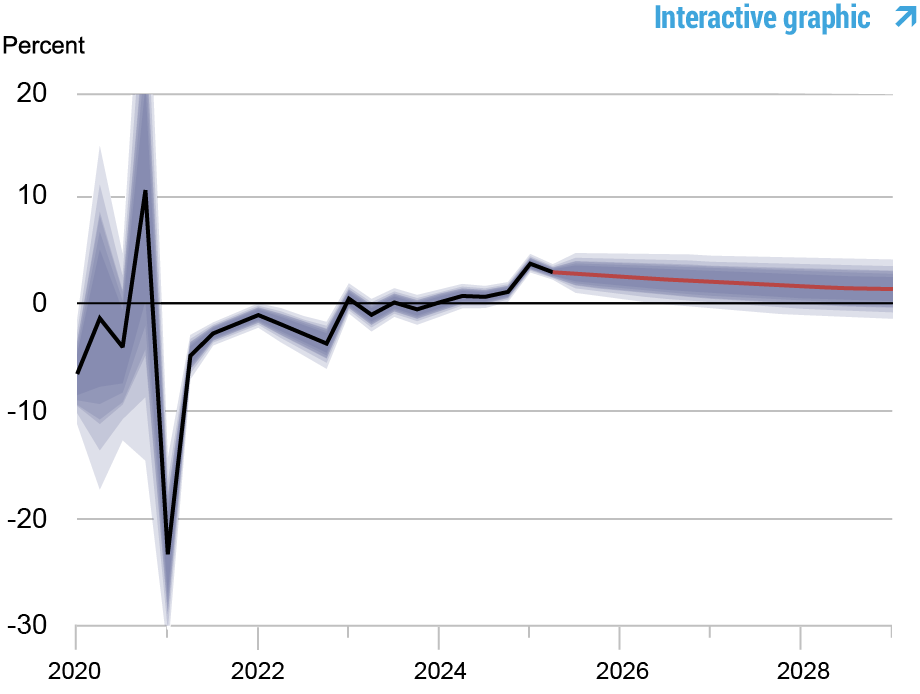

Real Natural Rate of Interest

Source: Authors’ calculations. Notes: The black line shows the model’s mean estimate of the real natural rate of interest; the red line shows the model forecast of the real natural rate. The shaded area marks the uncertainty associated with the forecasts at 50, 60, 70, 80, and 90 percent probability intervals.

Marco Del Negro is an economic research advisor in the Federal Reserve Bank of New York’s Research and Statistics Group.

Keshav Dogra is an economic research advisor in the Federal Reserve Bank of New York’s Research and Statistics Group.

Elena Elbarmi is a research analyst in the Federal Reserve Bank of New York’s Research and Statistics Group.

Donggyu Lee is a research economist in the Federal Reserve Bank of New York’s Research and Statistics Group.

Michael Pham is a research analyst in the Federal Reserve Bank of New York’s Research and Statistics Group.

How to cite this post:

Marco Del Negro, Keshav Dogra, Elena Elbarmi, Donggyu Lee, and Michael Pham, “The New York Fed DSGE Model Forecast—June 2026,” Federal Reserve Bank of New York Liberty Street Economics, June 22, 2026, https://libertystreeteconomics.newyorkfed.org/2026/06/the-new-york-fed-dsge-model-forecast-june-2026/

BibTeX: View |

@article{DelNegroDograElbarmiLeePham2026,

author={Del Negro, Marco and Dogra, Keshav and Elbarmi, Elena and Lee, Donggyu and Pham, Michael},

title={The New York Fed DSGE Model Forecast—June 2026},

journal={Liberty Street Economics},

note={Liberty Street Economics Blog},

number={June 22},

year={2026},

url={https://libertystreeteconomics.newyorkfed.org/2026/06/the-new-york-fed-dsge-model-forecast-june-2026/}

}

Disclaimer The views expressed in this post are those of the author(s) and do not necessarily reflect the position of the Federal Reserve Bank of New York or the Federal Reserve System. Any errors or omissions are the responsibility of the author(s).

]]>0<![CDATA[The Unintended Effects of Interest Rate Caps: Credit Reallocation to Safer Borrowers]]>https://libertystreeteconomics.newyorkfed.org/?p=427232026-06-03T18:03:28Z2026-06-03T11:01:00ZStaff Report, we study how these interventions have played out in three states. In our first post about that study, we showed that rate caps lead riskier borrowers to face rationing in the credit market. One question that naturally arises is what lenders do with the credit they used to provide to high-risk borrowers before the caps were imposed. Lenders that lend exclusively to high-risk borrowers (at rates above the cap) may decide to stop lending to high-risk borrowers in that state. Others, however, may try to change their “credit box” by lending more to somewhat safer borrowers. In this post, we will try to understand how lenders reallocate credit after usury limits are implemented.]]>

Rajashri Chakrabarti, Gabriel Leonard, Donald P. Morgan, Thu Pham, and Lee Seltzer

Several states have recently capped consumer loan rates with the stated purpose of protecting borrowers. In a recent Staff Report, we study how these interventions have played out in three states. In our first post about that study, we showed that rate caps lead riskier borrowers to face rationing in the credit market. One question that naturally arises is what lenders do with the credit they used to provide to high-risk borrowers before the caps were imposed. Lenders that lend exclusively to high-risk borrowers (at rates above the cap) may decide to stop lending to high-risk borrowers in that state. Others, however, may try to change their “credit box” by lending more to somewhat safer borrowers. In this post, we will try to understand how lenders reallocate credit after usury limits are implemented.

Rationing versus Re-allocation

While credit rationing under usury limits is clearly predicted by textbook economic theory, reallocation is less obvious. After all, if lending more to safer borrowers is profitable with a rate cap, why not do so without a cap? Based on the simple model provided in the last post, rate caps on high-risk borrowers should not affect borrowers with higher risk scores that have access to traditional credit markets. However, lenders may not be able to lend to both high-risk and low-risk borrowers due to limited access to capital, and some will find it more profitable to concentrate on high-risk borrowers. When the usury limits are put in place, lenders who had previously chosen to focus on high-risk borrowers may reallocate their capital to safer borrowers.

Some existing theoretical work supports this view. For instance, an early analysis by Blitz and Lang (1965) shows that under certain conditions, lenders will reallocate credit to moderate-risk borrowers when facing a usury limit: “it is the less risky borrowers…who are most likely to benefit from usury limits.” Indeed, Adam Smith, of all people, favored usury limits so more credit would flow from “prodigals and projectors” toward more “sober” borrowers.

There is empirical evidence of credit reallocation as well. Hodenborn finds usury limits in the 19th century led banks to favor safer borrowers “to the detriment of small, subprime borrowers.” A study of usury limits in Peru found that banks made fewer small loans and more medium-sized ones, “favoring incumbent firms at the expense of new borrowers.” Our paper looks for evidence of credit reallocation in the context of a modern usury limit in the U.S.

Our Study

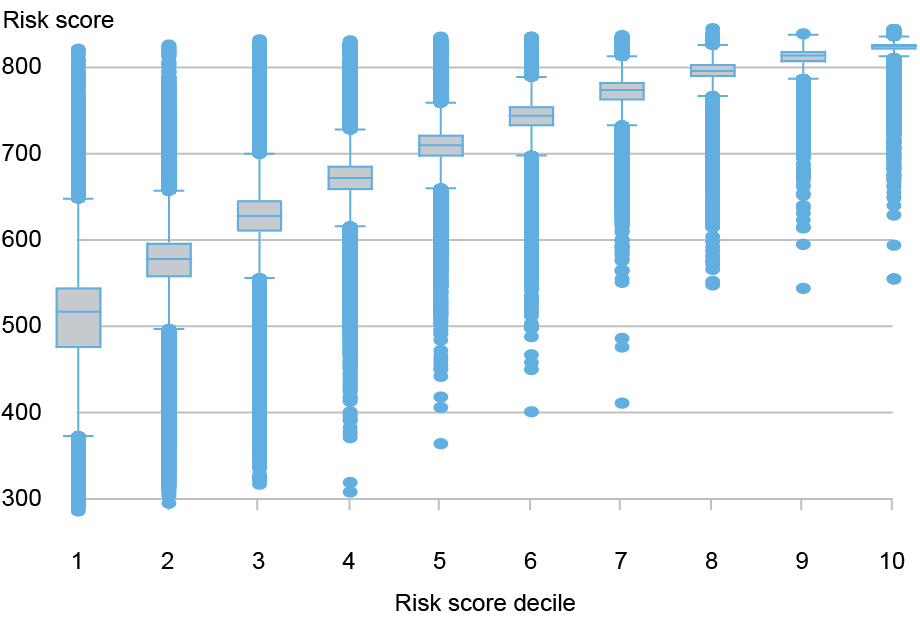

We examined how credit changed in three states that enacted 36 percent rate caps sometime between 2016 and 2022 (Illinois, South Dakota, and North Dakota). Our credit data are from the New York Fed Consumer Credit Panel/Equifax (CCP). The CCP tracks quarterly credit profiles for an anonymized random sample of 5 percent of households covered by the Equifax credit bureau. The sample comprises over 35 million borrowers. We measure borrower creditworthiness with the Equifax Risk Score 3.0; scores range between 350 and 800 and increase with creditworthiness.

The chart below displays the distribution of risk scores for the three states that enacted a usury limit between 2016 and 2022. Specifically, the chart shows the breakdown of borrowers within each risk score decile, showing the detailed distribution of risk scores within each decile. The risk score deciles are defined based on risk scores in the year before the usury limit passed (see our Staff Report for details). The median risk score in the lowest decile is about 518.

Risk Scores in the Lowest Decile Are About 150 Points Below Prime on Average

Sources: New York Fed Consumer Credit Panel/Equifax; authors’ calculations. Notes: This chart shows the distribution of risk scores by risk score decile for households in Illinois, North Dakota, and South Dakota; households with the lowest scores are in the first decile. Risk scores are as of the year before usury limits took effect. The center line in each box represents the median score in that decile. The top and bottom of each box represent the 25th and 75th percentiles of risk scores, respectively, in that decile. The interquartile range is the difference between the 75th and 25th quartiles.

In the absence of interest rate caps, high-cost lenders specialize in extending credit to higher-risk (low risk score) borrowers that are generally avoided by traditional, more risk-averse lenders such as banks and credit unions. In the presence of usury limits, these lenders may instead choose to lend more to slightly more creditworthy borrowers, for whom the usury limit does not bind. For instance, the median risk score in the third decile is around 620, which is the traditional cutoff for whether a borrower is subprime or prime. Lenders may extend newly available credit to prime borrowers after usury limits make lending to subprime borrowers unprofitable.

The chart below shows the increase in borrowing over time for the third risk score decile relative to all higher deciles. Similar increases in borrowing are observed in the fourth and fifth risk score deciles relative to all higher deciles. The results from these graphical analyses are consistent with lenders reallocating credit to relatively more creditworthy borrowers after the imposition of usury limits. Further consistent with this view, in the Staff Report we show that while borrowing declines substantially for borrowers in the lowest risk score decile, only a marginal decline is observed in the aggregate. This indicates that the increase in lending to borrowers in the third through fifth risk score deciles mostly offsets the decline in lending to borrowers in the second risk score decile.

Borrowers in the Middle of the Risk Score Distribution See Increased Lending after Rate Caps Relative to Control States

Sources: New York Fed Consumer Credit Panel/Equifax; authors’ calculations. Note: This chart shows how debt balances changed for borrowers in the third risk decile in Illinois, North Dakota, and South Dakota relative to their counterparts in control states.

Conclusion

In the previous post, we found that lenders reduce credit to the least creditworthy borrowers after usury limits are imposed. In this post, we show evidence that lenders simultaneously increase credit to marginally more creditworthy borrowers. Whether this reallocation was an intention of the proposer of the limits is unclear. In any case, our results imply that there may be tradeoffs involved in enacting usury limits, with some borrowers facing more adverse outcomes as others benefit.

Rajashri Chakrabarti is an economic research advisor in the Federal Reserve Bank of New York’s Research and Statistics Group.

Gabriel Leonard is a research analyst in the Federal Reserve Bank of New York’s Research and Statistics Group.

At the time this post was written, Donald P, Morgan was a financial research advisor in the Federal Reserve Bank of New York’s Research and Statistics Group. He is now retired.

Thu Pham is a research analyst in the Federal Reserve Bank of New York’s Research and Statistics Group.

Lee Seltzer is a financial research economist in the Federal Reserve Bank of New York’s Research and Statistics Group.

How to cite this post:

Rajashri Chakrabarti, Gabriel Leonard, Donald P. Morgan, Thu Pham, and Lee Seltzer, “The Unintended Effects of Interest Rate Caps: Credit Reallocation to Safer Borrowers,” Federal Reserve Bank of New York Liberty Street Economics, June 3, 2026, https://doi.org/10.59576/lse.20260603bBibTeX: View |

@article{ChakrabartiLeonardMorganPhamSeltzer2026,

author={Chakrabarti, Rajashri and Leonard, Gabriel and Morgan, Donald P. and Pham, Thu and Seltzer, Lee},

title={The Unintended Effects of Interest Rate Caps: Credit Reallocation to Safer Borrowers},

journal={Liberty Street Economics},

note={Liberty Street Economics Blog},

number={June 3},

year={2026},

url={https://doi.org/10.59576/lse.20260603b}

}

Disclaimer The views expressed in this post are those of the author(s) and do not necessarily reflect the position of the Federal Reserve Bank of New York or the Federal Reserve System. Any errors or omissions are the responsibility of the author(s).

]]>0<![CDATA[The Unintended Effects of Interest Rate Caps: Credit Rationing for Risky Borrowers]]>https://libertystreeteconomics.newyorkfed.org/?p=427082026-06-03T18:02:54Z2026-06-03T11:00:00Zlight cane.” (Rockoff 2003) Centuries later, many U.S. states are imposing the same cap (without corporal penalties) on alternative credit providers, such as payday, installment, and auto-title lenders, with the goal of lowering credit costs and delinquency for the high-risk borrowers that rely on these funding sources. A concern, however, is that lenders will simply refuse to lend to these borrowers at lower interest rates. Our recent Staff Report studies how interest rate caps have played out in several states that recently adopted them. Using household-level data from a major credit bureau, we find that loan balances for the riskiest borrowers declined substantially relative to counterparts in states without caps. Despite taking on less debt, these borrowers did not experience an improvement in delinquencies.]]>

Rajashri Chakrabarti, Gabriel Leonard, Donald P. Morgan, Thu Pham, and Lee Seltzer

In imperial China, 3 percent was the maximum legal monthly loan rate; charging more was punishable by 40 to 100 blows with the “light cane.” (Rockoff 2003) Centuries later, many U.S. states are imposing the same cap (without corporal penalties) on alternative credit providers, such as payday, installment, and auto-title lenders, with the goal of lowering credit costs and delinquency for the high-risk borrowers that rely on these funding sources. A concern, however, is that lenders will simply refuse to lend to these borrowers at lower interest rates. Our recent Staff Report studies how interest rate caps have played out in several states that recently adopted them. Using household-level data from a major credit bureau, we find that loan balances for the riskiest borrowers declined substantially relative to counterparts in states without caps. Despite taking on less debt, these borrowers did not experience an improvement in delinquencies.

The Resurgence of Usury Limits

Usury limits have waned over the centuries in the U.S, but their recent resurgence on the consumer side was triggered by payday lenders’ entry into the small dollar loan market in the mid-1990s (Rockoff 2003). In 2007, rates on loans to military staff were capped at 36 percent—marking the first-ever national usury limit in the U.S. A bill currently before Congress, the Predatory Loan Elimination Act, would extend the 36 percent cap across the entire U.S.

Saunders (2021) traces the 36 percent standard back to credit reform in the early 20th century. Concerned that prevailing usury limits were too low, the Russell Sage Foundation promulgated a Uniform Small Loan Law recommending a higher cap of 3.5 percent per month. Thirty-four states raised caps to between 36 and 42 percent over the next few decades (Anderson et al. 2015).

Cheaper Credit…or Less Credit?

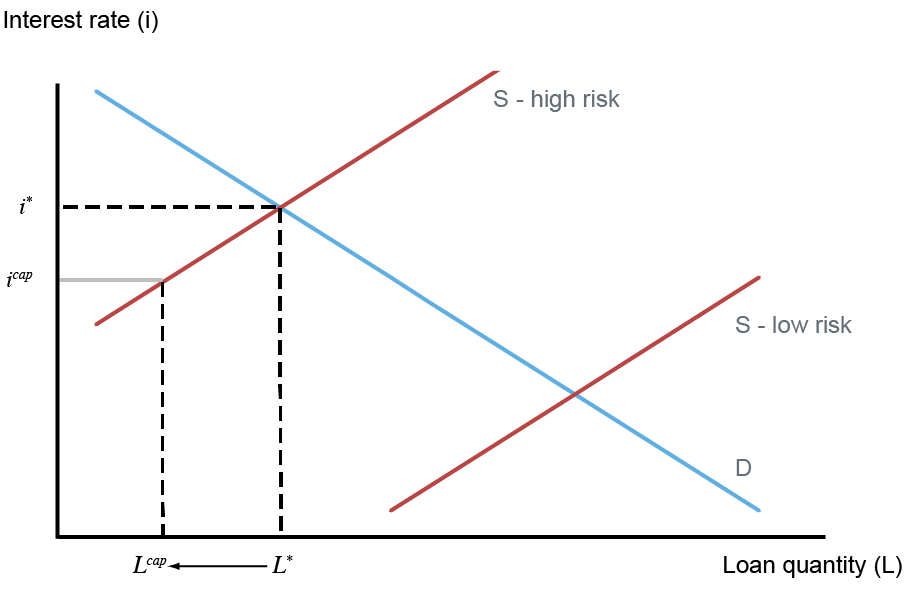

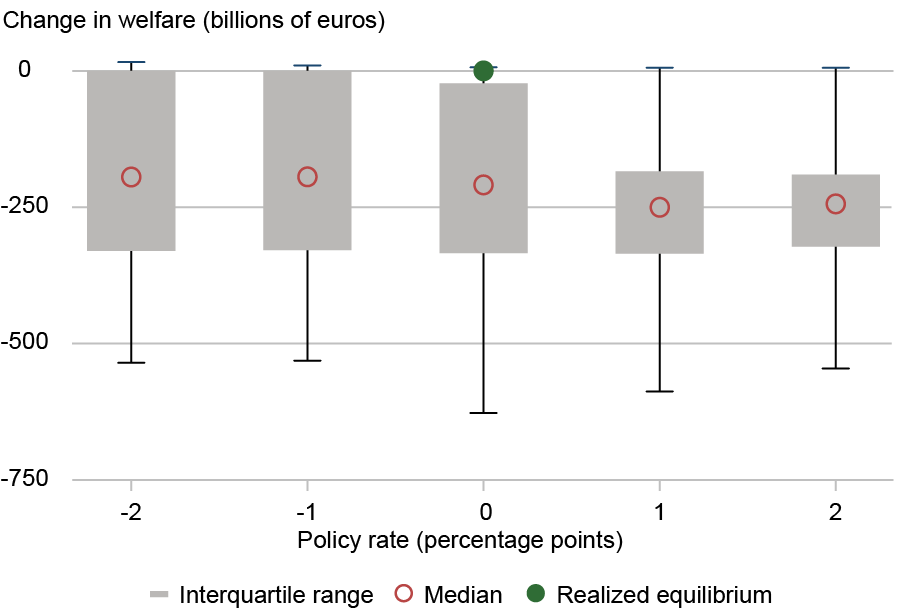

Opponents of rate caps predict that they will lower the supply of credit for riskier borrowers rather than drive down the cost of credit. The textbook credit model below illustrates this effect. In this model, lenders separately provide credit for high-risk borrowers (sH) and low-risk borrowers (sL). At market equilibrium, lenders charge high-risk borrowers i*, which is higher than what they would charge low-risk borrowers; lenders charge high-risk borrowers a higher interest rate to compensate for higher expected loan losses. However, a usury cap requires lenders to charge no higher than icap for interest, which is lower than the equilibrium rate i*. As a result, lenders contract the quantity of loans supplied, as shown. In fact, if profits from loans to high-risk borrowers don’t cover the fixed cost of providing them, lenders may entirely refuse to make any loans to high-risk borrowers, which is referred to as credit rationing. This is particularly likely as less creditworthy borrowers are also typically more likely to take out relatively small loans.

Note that icap is higher than the equilibrium interest rate for low-risk borrowers, and under standard model assumptions, lending to lower-risk borrowers does not change. However, under certain conditions, the rate cap could also have implications for low-risk borrowers, a situation we examine in the next post in this series.

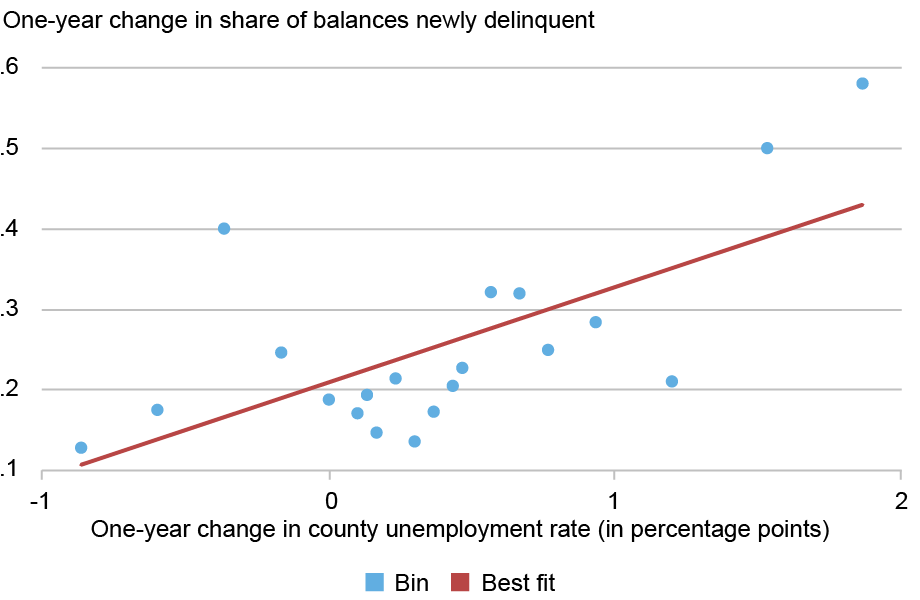

Rate Caps May Contract Credit to Riskier Borrowers

Source: Authors’ rendering. Notes: This chart shows a simple model of consumer lending and illustrates how a usury cap would affect the market. There are two types of borrowers—high-risk and low-risk—and supply of credit is separately determined for high- (sH) and low-risk borrowers (sL). At equilibrium, high-risk borrowers are able to borrow L* dollars of loans, at an interest rate of i*. Under the usury cap, lenders can only charge icap, and as a result reduce the quantity of loans supplied to Lcap.

Our Study

We examined how credit changed in three states that enacted 36 percent rate caps sometime between 2016 and 2022 (Illinois, South Dakota, and North Dakota). Only alternative lenders’ loan rates are capped; banks and credit unions are exempt. Our data are from the New York Fed Consumer Credit Panel/Equifax (CCP), which tracks quarterly debt and delinquency for an anonymized, random subset of households covered by the Equifax credit bureau. Comprising 5 percent of Equifax-monitored households, the sample includes over 35 million borrowers.

Since rate caps are more likely to bind for riskier borrowers, we sorted households into ten equal-sized groups (deciles) based on their credit scores (Equifax Risk Score 3.0), with the lowest-scoring borrowers in the first decile. The average loan delinquency rate for this group was over six times higher than the average across the other deciles.

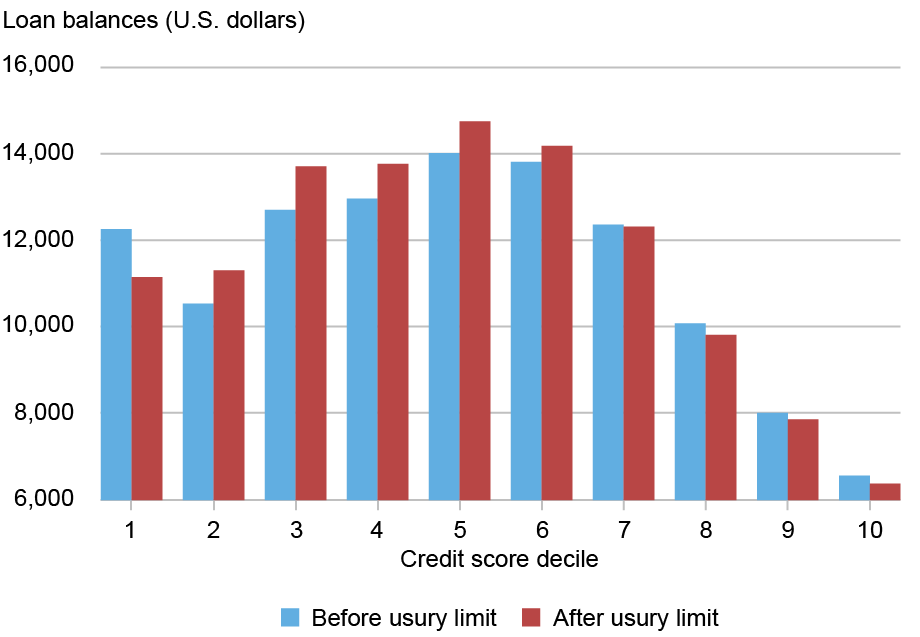

To get a sense of the data, the chart below shows average loan balances for borrowers in the states with usury limits (excluding mortgages and student loans) for each risk decile. Predictably, households with the lowest and highest scores owe less. More relevant is that balances declined by about 8 percent for the first (riskiest) decile after rates were capped; balances for safer borrowers were little changed overall.

Loan Balances for the Riskiest Borrowers Declined After Rate Caps

Sources: New York Fed Consumer Credit Panel/Equifax; authors’ calculations. Notes: This chart shows how average loan balances for households in Illinois, North Dakota, and South Dakota changed after loan rates were capped in those states. Households are stratified by credit score decile, with decile 1 containing those with the lowest scores. Mortgage and student loans are excluded.

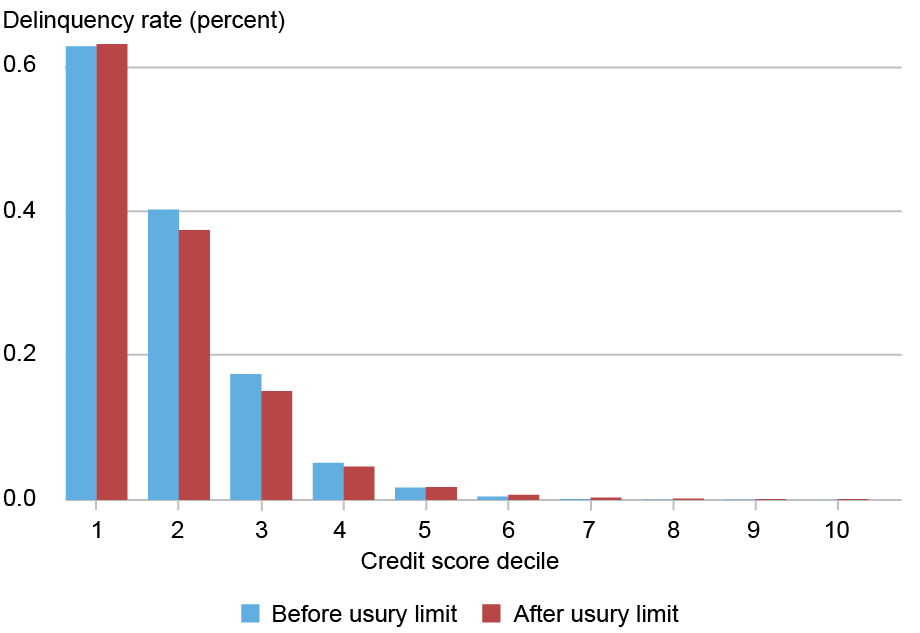

Lower debt balances might be salutary if they reflect that riskier borrowers are avoiding “debt traps.” Yet rate caps did not lead to fewer delinquencies for those borrowers, as the chart below shows. Their share of delinquent accounts (90+ days overdue) was essentially unchanged, while delinquency for somewhat lower-risk households tended to fall.

Loan Delinquency Among the Riskiest Borrowers Did Not Decline After Usury Limits

Sources: New York Fed Consumer Credit Panel/Equifax; authors’ calculations. Notes: This chart shows how delinquency rates for households in Illinois, North Dakota, and South Dakota changed after loan rates were capped in those states. Households are stratified by credit score decile, with decile 1 containing those with the lowest scores. Delinquency is measured by the share of accounts that are 90+ days overdue. Delinquencies on all types of debt are included in the chart.

Cross-State Comparison

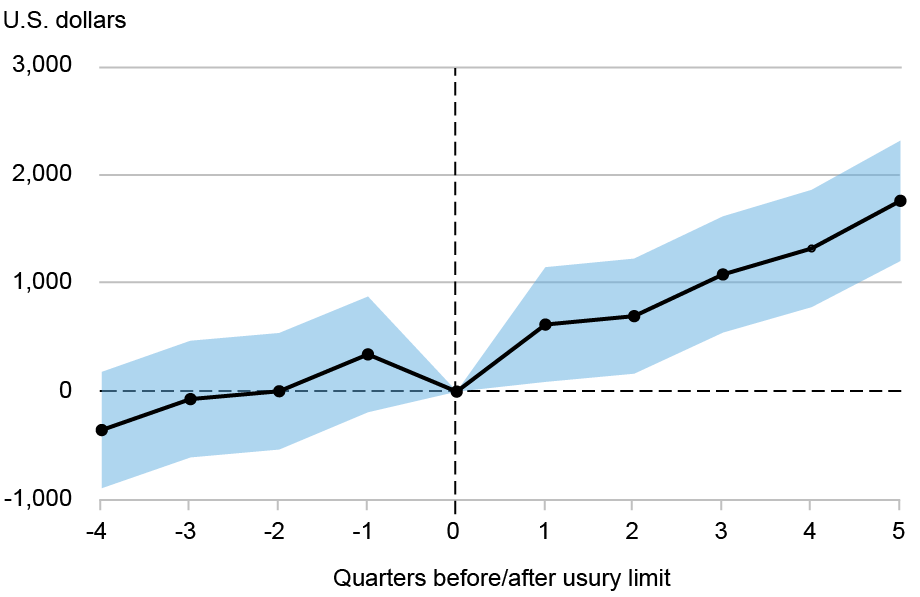

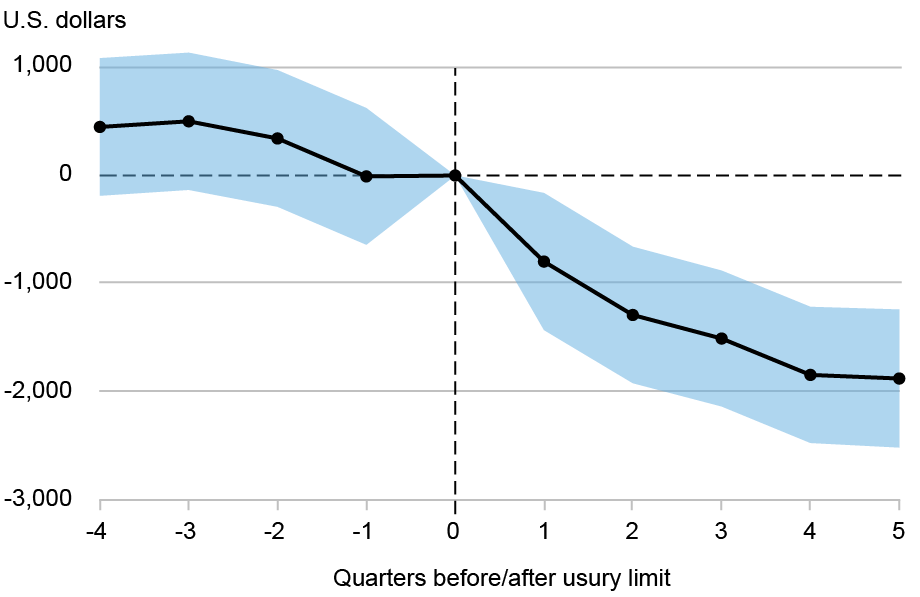

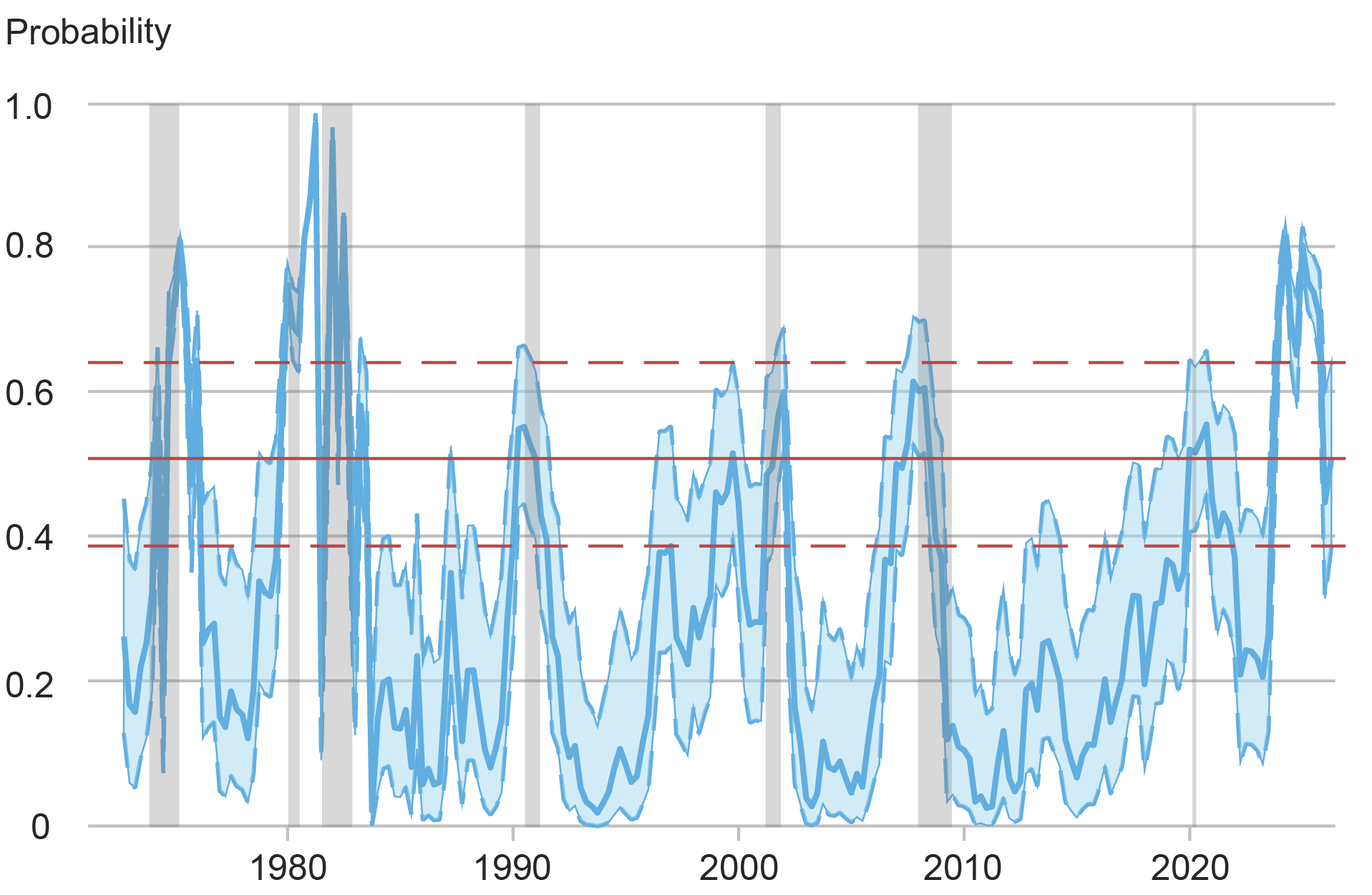

The charts above only show changes in credit for borrowers in the states that capped rates. In our main analysis, we compare borrowers in those states to counterparts in a set of control states that did not cap rates over the study period. Using regression analysis, we estimate how credit for high-risk borrowers in the treated states changed relative to counterparts after rate caps took effect, where high-risk borrowers are defined as those who were in the lowest decile of risk scores before the usury limit. In particular, we estimate an event-study regression to examine how credit market outcomes changed for high-risk borrowers in states with usury limits, relative to control with no usury limit. Importantly, these regressions allow us to control for changes over time happening in each state that are unrelated to the usury limit, and for differences between borrowers unrelated to the usury limit.

The estimates for loan balances are plotted below, along with confidence intervals. Relative to control state levels, the average loan balances of the riskiest borrowers in rate-cap states were not significantly different before those caps took effect, which indicates that the control groups used in this study offer a reasonable point of comparison. However, they declined significantly afterward. The effect is substantial. Specifically, as of five quarters after rates are capped, debt balances of the riskiest borrowers in those states fall by around $2,000, relative to the balances of the riskiest borrowers in control-states.

Balances for the Riskiest Borrowers Decline After Rate Caps Relative to Control States

Sources: New York Fed Consumer Credit Panel/Equifax; authors’ calculations. Note: This chart shows how the debt balances of high-risk borrowers in Illinois, North Dakota, and South Dakota changed after the implementation of usury limits in those states, relative to the debt balances of their counterparts in control states.

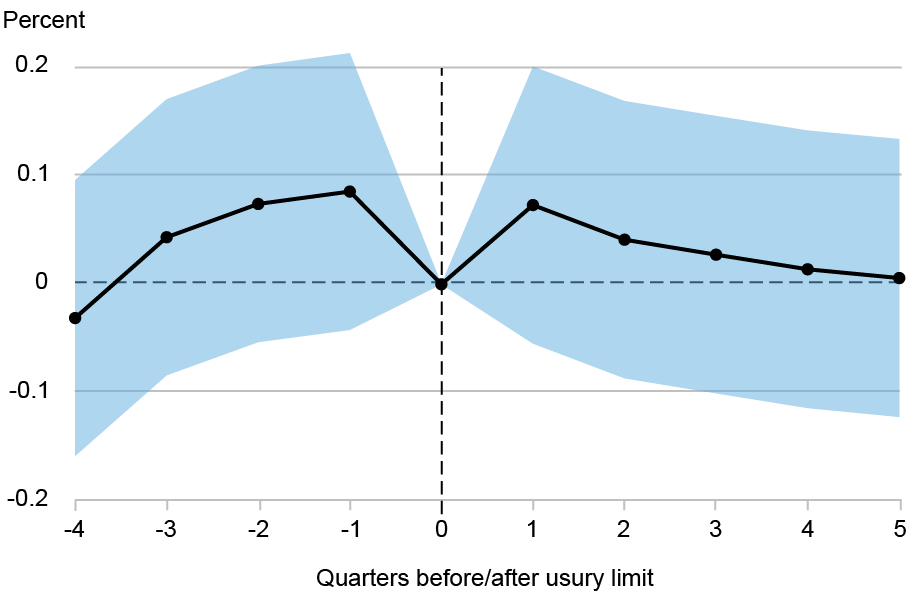

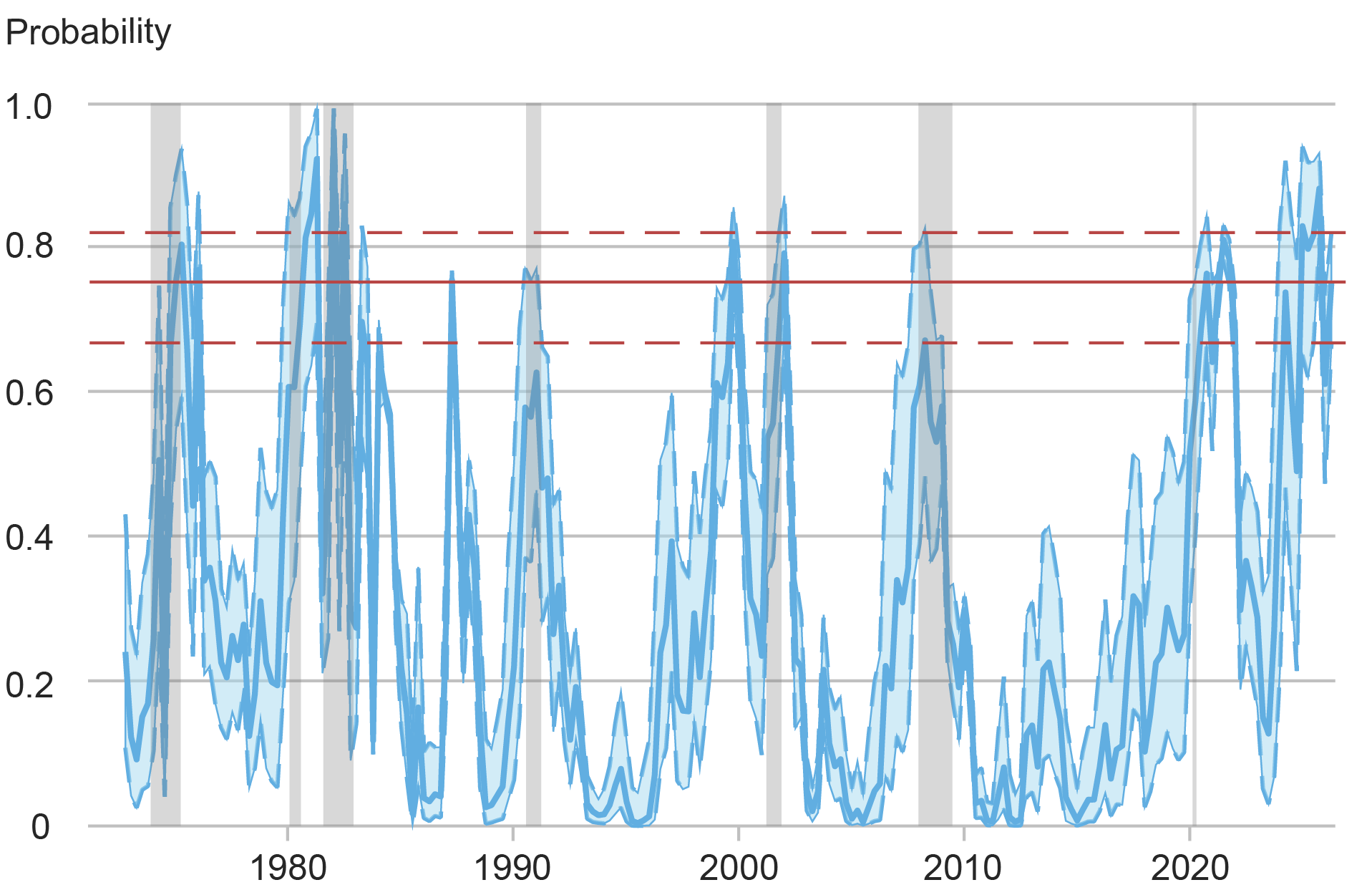

The next chart shows how relative delinquencies evolved. These estimates are less precise (as reflected in the wide confidence bands), but they certainly do not point to a decline in delinquencies. Overall, it seems that there was no change in delinquencies for the riskiest borrowers in states with usury limits relative to those in control states after the usury limits were passed.

Delinquency Rates of Riskiest Borrowers Hold Steady Relative to Control States

Sources: New York Fed Consumer Credit Panel/Equifax; authors’ calculations. Note: This chart shows how the probability of having a delinquent loan changed for high-risk borrowers in Illinois, North Dakota, and South Dakota after the implementation of usury limits in those states, relative to delinquency rates for their counterparts in control states.

Summing Up

Usury limits, an ancient type of financial regulation, are resurgent in the U.S. Advocates expect rate caps to lower borrowing costs for high-risk borrowers while opponents predict that the result will be less credit for these borrowers. Our findings square better with the latter view, calling into question the benefits of these laws for high-risk borrowers. In our next post, we examine whether lenders reallocate credit to somewhat lower-risk borrowers in response to rate caps.

Rajashri Chakrabarti is an economic research advisor in the Federal Reserve Bank of New York’s Research and Statistics Group.

Gabriel Leonard is a research analyst in the Federal Reserve Bank of New York’s Research and Statistics Group.

At the time this post was written, Donald P, Morgan was a financial research advisor in the Federal Reserve Bank of New York’s Research and Statistics Group. He is now retired.

Thu Pham is a research analyst in the Federal Reserve Bank of New York’s Research and Statistics Group.

Lee Seltzer is a financial research economist in the Federal Reserve Bank of New York’s Research and Statistics Group.

How to cite this post:

Rajashri Chakrabarti, Gabriel Leonard, Donald P. Morgan, Thu Pham, and Lee Seltzer, “The Unintended Effects of Interest Rate Caps: Credit Rationing for Risky Borrowers,” Federal Reserve Bank of New York Liberty Street Economics, June 3, 2026, https://doi.org/10.59576/lse.20260603aBibTeX: View |

@article{ChakrabartiLeonardMorganPhamSeltzer2026,

author={Chakrabarti, Rajashri and Leonard, Gabriel and Morgan, Donald P. and Pham, Thu and Seltzer, Lee},

title={The Unintended Effects of Interest Rate Caps: Credit Rationing for Risky Borrowers},

journal={Liberty Street Economics},

note={Liberty Street Economics Blog},

number={June 3},

year={2026},

url={https://doi.org/10.59576/lse.20260603a}

}

Disclaimer The views expressed in this post are those of the author(s) and do not necessarily reflect the position of the Federal Reserve Bank of New York or the Federal Reserve System. Any errors or omissions are the responsibility of the author(s).

]]>0<![CDATA[Struggling Regional Small Businesses Deeply Pessimistic About 2026 Prospects]]>https://libertystreeteconomics.newyorkfed.org/?p=429442026-06-02T18:24:41Z2026-06-02T11:00:00Zsuite of indicators describing the performance of small businesses in the Second District (defined, for the purpose of this study, as New York, New Jersey, and Connecticut) and nationally with data from the 2025 edition of the Small Business Credit Survey (SBCS). In this post, we find that regional small businesses reported severe declines in employment and revenue growth in 2025 and became more pessimistic about growth in 2026. In contrast, small firms in the rest of the nation enjoyed stable revenues and employment in 2025 and, while they also had lower expectations of future growth, the decline was smaller in magnitude. Given the importance of small businesses in employment generation, analyzing such data helps to inform the design of effective monetary policy and to understand trends in the regional economy.]]>

Will Aarons and Asani Sarkar

We recently updated the suite of indicators describing the performance of small businesses in the Second District (defined, for the purpose of this study, as New York, New Jersey, and Connecticut) and nationally with data from the 2025 edition of the Small Business Credit Survey (SBCS). In this post, we find that regional small businesses reported severe declines in employment and revenue growth in 2025 and became more pessimistic about growth in 2026. In contrast, small firms in the rest of the nation enjoyed stable revenues and employment in 2025 and, while they also had lower expectations of future growth, the decline was smaller in magnitude. Given the importance of small businesses in employment generation, analyzing such data helps to inform the design of effective monetary policy and to understand trends in the regional economy.

What Is New and Relevant About Small Business Indicators?

The New York Fed small business indicators leverage data from the Small Business Credit Survey (SBCS), an annual survey of business owners with fewer than 500 employees by the twelve Federal Reserve Banks. We focus on employer firms—that is, firms with at least one employee other than the owner. In addition to reviewing performance indicators for small businesses nationally (also provided in the SBCS 2026 report), we show how these indicators vary by firm size and compare indicators for small businesses in the Second District with their national counterparts.

Profitability, Revenues, and Costs

Revenue performance in 2025 was worse for regional firms as compared to national firms. Relative to 2024, revenues in 2025 were similar for national firms but worsened by more than 8 percentage points for regional firms. Moreover, lower revenues in 2025 were driven by the smallest firms (with fewer than ten employees) nationally but by firms of all sizes regionally.

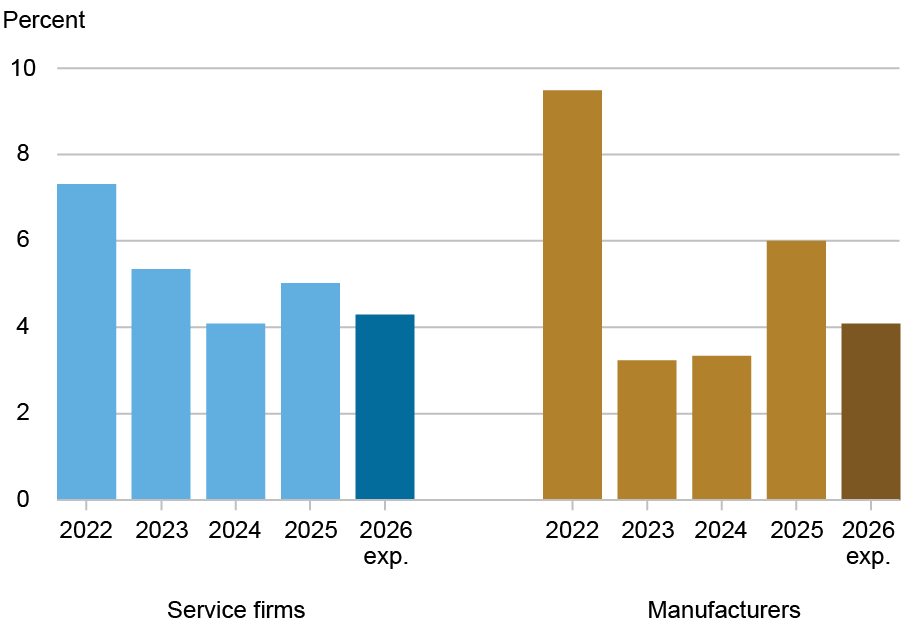

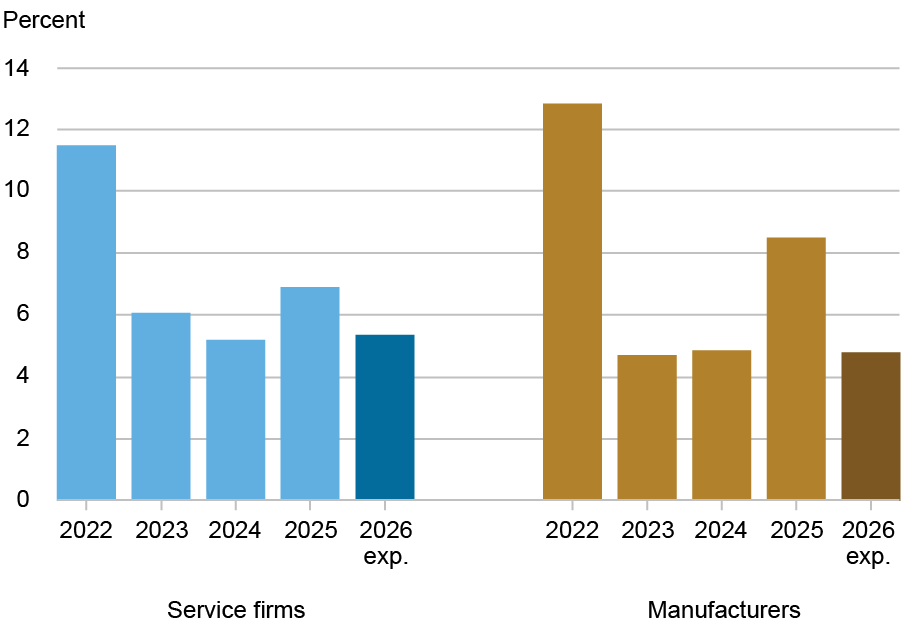

Revenue expectations for 2026 were notably pessimistic (see chart below). Revenue expectations for all size groups declined by 6 percentage points year-over-year for national firms, and an astounding 20 to 30 percentage points for regional firms. These numbers are the worst recorded in the survey since 2020 both at the national and regional levels.

Expected Change in Revenues for 2026 Declined Sharply for Regional Small Businesses

Percent

Sources: Federal Reserve Banks, 2019-2025 Small Business Credit Surveys. Notes: The chart plots the diffusion index (percentage expecting an increase minus percentage expecting a decrease) of responses to the question: “How does your business expect its revenue to change over the next 12 months?” The total number of respondents by year was: 2019, 4,967; 2020, 9,616; 2021, 10,692; 2022, 7,674; 2023, 5,945; 2024, 7,456; 2025, 6,389.

Profitability numbers in the survey are more backward looking, as they are a snapshot of conditions in December 2024. National firms reported profits 13 percentage points more often than losses while regional firms did so 8 percentage points more often. Thus, in contrast to revenues, profitability increased for firms of all sizes, perhaps reflecting better conditions for small businesses in 2024 than 2025. Despite the improvements, profitability remains far below the pre-pandemic differential of 46 percentage points for national firms and 41 percentage points for regional firms in December 2019.

As in the prior year’s survey, fewer firms in the national sample reported higher input and wage costs as a financial challenge in recent years.

Employment

Like their poorer revenue conditions, the employment performance of regional firms was also worse than that of national firms in 2025. Year-over-year employment growth held steady for all national firms except for the larger ones (with ten or more employees), which have exhibited weakening employment recovery after 2022. In contrast, employment growth fell for regional firms of all sizes in 2025, decreasing by 9 percentage points overall.

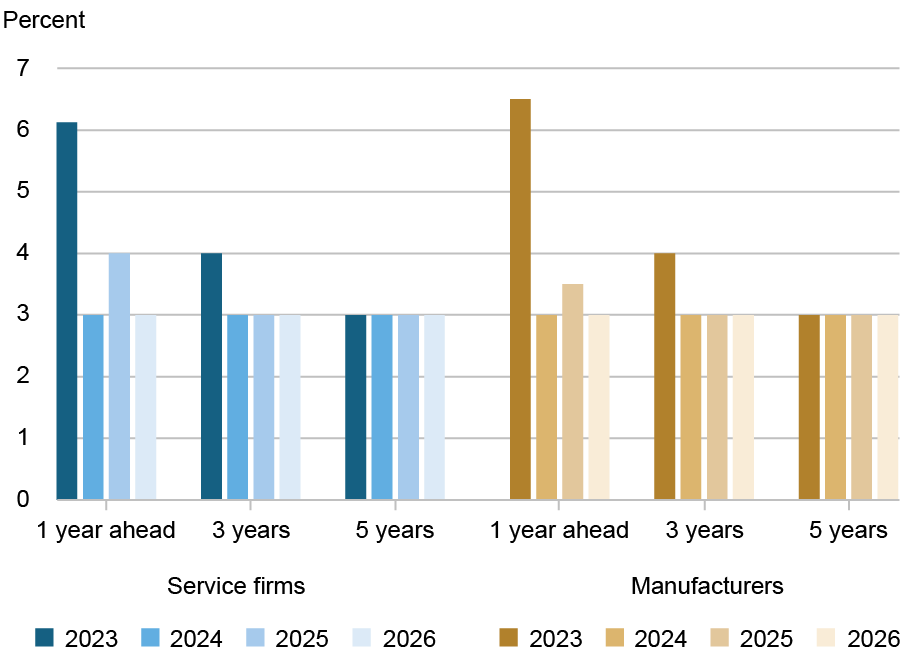

Mirroring pessimistic revenue expectations, a lower share of firms of all sizes expected higher employment growth in 2026 relative to recent years. However, the magnitude of declining expectations was markedly higher for regional as compared to national firms. Thus, the net share of firms expecting to generate employment in 2026, relative to 2025, declined by 16 percentage points for regional firms but less than 4 percentage points for national firms (see chart below). Indeed, for the first time in the survey, large regional firms expected negative employment growth. These results are part of an ongoing pattern whereby firms in the region have struggled to generate employment since the pandemic.

Expected Change in Employment for 2026 Declined Sharply for Regional Small Businesses

Percent

Sources: Federal Reserve Banks, 2019-2025 Small Business Credit Surveys. Notes: The chart plots the diffusion index (percentage expecting an increase minus percentage expecting a decrease) of responses to the question: “How does your business expect its employment to change over the next 12 months?” The total number of respondents by year was: 2019, 4,967; 2020, 9,616; 2021, 10,692; 2022, 7,674; 2023, 5,945; 2024, 7,456; 2025, 6,389.

Indebtedness

Debt (defined as the mid-point of the range reported by respondents) in 2025 was about $67,000 per employee for national firms, similar to 2024, and $81,000 per employee for regional firms, a small increase from 2024. Similar shares of firms received less than the full amount of credit that they applied for and reported that they did not apply for credit because they did not need funds as in 2024, suggesting that credit supply was typically not a major constraint in 2025.

Technology and Supply Chain

In the region, more firms of all sizes reported difficulties with utilizing technology while the share of firms reporting supply chain issues continued to decline both nationally and regionally.

Summing Up

Using annual survey data, we report on national and Second District trends in small business performance from 2019 to 2025. We find that Second District firms continued to struggle to generate revenues and employment and were deeply pessimistic of their prospects in 2026. In no other major U.S. state were small business expectations for 2026 so downbeat (other than revenue expectations in Massachusetts). While national firms also lowered their expectations of employment and revenue growth in 2026, the decline was smaller in magnitude than that of regional firms.

Will Aarons is a research analyst in the Federal Reserve Bank of New York’s Research and Statistics Group.

Asani Sarkar is a financial research advisor in the Federal Reserve Bank of New York’s Research and Statistics Group.

How to cite this post:

Will Aarons and Asani Sarkar, “Struggling Regional Small Businesses Deeply Pessimistic About 2026 Prospects,” Federal Reserve Bank of New York Liberty Street Economics, June 2, 2026, https://doi.org/10.59576/lse.20260602BibTeX: View |

@article{AaronsSarkar2026,

author={Aarons, Will and Sarkar, Asani},

title={Struggling Regional Small Businesses Deeply Pessimistic About 2026 Prospects},

journal={Liberty Street Economics},

note={Liberty Street Economics Blog},

number={June 2},

year={2026},

url={https://doi.org/10.59576/lse.20260602}

}

Disclaimer The views expressed in this post are those of the author(s) and do not necessarily reflect the position of the Federal Reserve Bank of New York or the Federal Reserve System. Any errors or omissions are the responsibility of the author(s).

]]>0<![CDATA[Remote Work Leaves Younger Workers Sidelined]]>https://libertystreeteconomics.newyorkfed.org/?p=428622026-06-02T15:48:31Z2026-06-01T14:30:00Z

Natalia Emanuel, Emma Harrington, and Amanda Pallais

Youth unemployment has risen dramatically since the pandemic—as has the prevalence of remote work. Our analysis suggests that these trends are related, with remote work making it more difficult for managers to train and mentor new employees. Accordingly, companies may be reluctant to hire less-experienced workers in distributed work arrangements. We estimate that remote work can explain 64 percent of the recent increase in unemployment among young college graduates. Further, the timing of this surge suggests that remote work—not generative AI—explains the bulk of the rise in youth unemployment.

(Not) Working from Home

Unemployment among young college graduates has risen significantly since the pandemic, a topic much discussed by scholars and the popular press. While unemployment among those under 29 was 3.1 percent on average in 2017-19, it rose by 20 percent to 3.7 percent in 2022-25.

The unemployment dynamics for young graduates particularly stand out given that the unemployment rate for more experienced college graduates actually dipped from 1.9 percent in 2017-19 to 1.8 percent in 2022-25. The chart below shows how unemployment evolved for college-educated workers of varying ages.

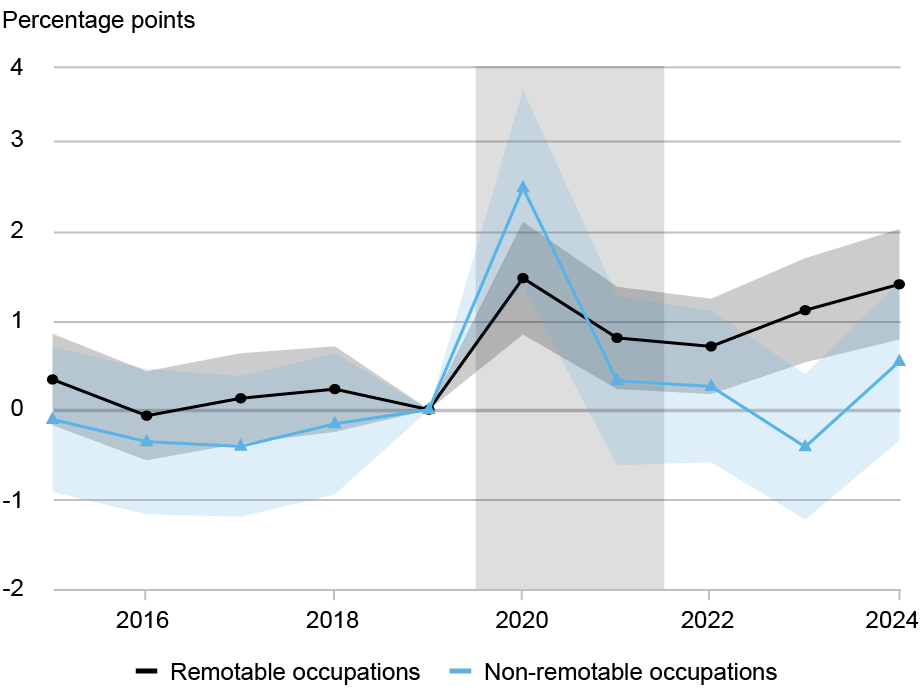

Unemployment among Young College Graduates Surges Above That of Experienced Workers

Percentage points

Source: Authors’ calculations from CPS data. Notes: Gray shading denotes the early pandemic period. Series show change in unemployment rates by age group relative to 2019 levels.

The high unemployment rates of young college graduates are particularly concerning because early-career experiences can have lasting consequences. For example, entering the labor market in a recession can scar a person’s career. Research finds that individuals who began looking for jobs in slacker labor markets tend to have lower earnings and slower career progression relative to comparable peers who began their job search in better market conditions.

Remote Job Prospects

We document that one factor contributing to youth unemployment is the four-fold rise in remote work since the pandemic. Employers may not want to hire fresh graduates onto distributed teams because it is more difficult to teach them the requisite skills from afar.

We compare unemployment rates among people working in “remotable” jobs—such as software engineering—to those in “non-remotable” jobs—such as mechanical engineering. To categorize an occupation as remotable or non-remotable, we use a commonly used index of how easily the tasks required for a given job can be done remotely. We then compare the unemployment rates of younger individuals in remotable and non-remotable jobs to those of more experienced workers.

The aggregate increase in the unemployment rate for young college graduates can be traced to remotable occupations, where young people’s unemployment rate increased by almost 1 percentage point between 2017-19 and 2022-24. By contrast, the unemployment rate of older workers in remotable sectors marginally declined over that period. As a result, the age gap in unemployment between younger and older workers significantly increased in remotable occupations. This relative increase in young people’s unemployment coincided with the pandemic and has remained elevated since then, as have rates of remote work.

By contrast, in non-remotable jobs, young graduates’ relative unemployment rate ticked up in 2020 but returned to baseline soon afterward. This divergence is illustrated in the chart below.

Unemployment Age Gap for College Graduates Driven by Job Remotability

Source: Authors’ calculations from CPS data. Notes: Gray shading denotes the early pandemic period. Series show the age gap (18-28 versus 29+) in unemployment rates by occupation category relative to 2019 levels.

Since so many young college graduates are in remotable occupations, our back-of-the-envelope calculation indicates that remote work can explain 64 percent of the increase in unemployment for all young college graduates between 2017−19 and 2022−24.

The AI Factor

Many analysts have attributed the recent labor market challenges of young college graduates to generative AI, among other factors. But the uptick in youth unemployment rates predates the rapid diffusion of AI. Moreover, even when we hold occupations’ exposure to AI constant, we find that the differences between younger and older workers persist in both remotable and non-remotable jobs.

Of course, generative AI and other factors may play a more primary role in determining the employment patterns of younger workers going forward. Nonetheless, the evidence to date suggests that the rise of remote work has meaningfully contributed to the recent challenges facing young college graduates.

Patterns at the Firm Level

Working with proprietary data from a Fortune 500 company, we are able to shed light on the underlying reasons for these labor market changes. We show that when people work next to their colleagues, they receive more feedback on their output and more mentorship. When they are separated even by a short distance, that feedback tapers off dramatically. The loss in feedback is more pronounced for younger workers, who miss out on constructive comments that spur their development.

The negative effects of operating remotely from one’s colleagues show up in work quality as well. When all employees functioned in isolation, those who had previously worked side-by-side with teammates, and consequently received more mentorship from their colleagues, produced better-quality output than those who had spent more time working at a distance from their teammates. Further, when we analyze the firm’s return-to-office (RTO) mandates, we find that workers on co-located teams, who experienced a more meaningful change in their proximity to colleagues, likewise showed greater improvements in their work quality.

The firm’s hiring patterns suggest that it understood the pitfalls of distance for worker development. When its offices were closed due to the pandemic, the firm hired fewer inexperienced workers and more experienced workers, who might need less mentorship to do their jobs well. Once its offices reopened, the company shifted back to hiring younger workers. However, there is a twist: for positions on distributed teams, the firm consistently hired more experienced workers, even after reopening. This divergence suggests that the firm’s hiring decisions were influenced by the complications of remote work rather than other macroeconomic trends. Overall, the firm’s hiring patterns suggest that it is willing to teach junior workers when proximity is feasible but shies away from employing inexperienced workers if distance creates barriers to training and development.

RTO and Job Opportunities

Consistent with our findings, many firms’ RTO mandates have cited the importance of colocation for mentorship and learning. The firm we study had a stricter RTO policy than other tech firms, which enabled it to mentor in-person and therefore hire young workers post-pandemic.

These dynamics suggest that remote work has weakened incentives to hire young workers by impeding on-the-job training. Ironically, when jobs are scarce, it becomes even harder for young workers to secure the training they need.

Natalia Emanuel is a research economist in the Federal Reserve Bank of New York’s Research and Statistics Group.

Emma Harrington is an assistant professor of economics at the University of Virginia.

Amanda Pallais is a professor of economics at Harvard University.

How to cite this post:

Natalia Emanuel, Emma Harrington, and Amanda Pallais, “Remote Work Leaves Younger Workers Sidelined,” Federal Reserve Bank of New York Liberty Street Economics, June 1, 2026, https://doi.org/10.59576/lse.20260601BibTeX: View |

@article{EmanuelHarringtonPallais2026,

author={Emanuel, Natalia and Harrington, Emma and Pallais, Amanda},

title={Remote Work Leaves Younger Workers Sidelined},

journal={Liberty Street Economics},

note={Liberty Street Economics Blog},

number={June 1},

year={2026},

url={https://doi.org/10.59576/lse.20260601}

}

Disclaimer The views expressed in this post are those of the author(s) and do not necessarily reflect the position of the Federal Reserve Bank of New York or the Federal Reserve System. Any errors or omissions are the responsibility of the author(s).

]]>3<![CDATA[The Regional Side of the Story: K‑Shaped Pattern in Region, Wider Gap in Gas Spending]]>https://libertystreeteconomics.newyorkfed.org/?p=428572026-05-28T13:09:19Z2026-05-28T14:00:00Zwe documented earlier. We find similar K‑shaped patterns in both retail and gas spending in our region as we do in the nation, with the K‑shaped pattern in gasoline in response to the recent gas price shock being more pronounced in the region.]]>

Rajashri Chakrabarti, Thu Pham, Beck Pierce, and Maxim L. Pinkovskiy

In this post, we use the inaugural release of our regional consumer spending indicators to ask whether these patterns hold for a significant portion of the Second District, and how regional spending patterns by income have been similar to or different from the national patterns we documented earlier. We find similar K‑shaped patterns in both retail and gas spending in our region as we do in the nation, with the K‑shaped pattern in gasoline in response to the recent gas price shock being more pronounced in the region.

Introducing the Regional Consumer Spending EHIs

This post accompanies the release of the Economic Heterogeneity Indicators (EHIs) through April 2026, which for the first time feature regional consumer spending indicators based on microdata from the market research firm Numerator. These indicators demonstrate our commitment to understanding how economic trends affect different segments of society not just in the nation, but in this region.

To create the regional consumer spending EHIs, we narrow the panel to participants in Numerator’s sample who live in zip codes within a significant portion of the Second District (New York State, northern New Jersey, and Fairfield County, CT. The Numerator panel does not cover Puerto Rico or the Virgin Islands). We verify the demographics of the panel participants to closely match the demographics of the Second District in the American Community Survey (ACS). We also verify that aggregate growth rates of retail spending excluding autos and excluding nonstore spending using the Numerator data for New York State and New Jersey closely match the corresponding growth rates in the Advance Monthly Retail Trade Survey (MARTS ). We are therefore confident that our Second District consumer spending indicators can be trusted to give us accurate trends for different demographic groups within the Second District.

To obtain real Second District spending growth rates, we deflate retail and gas spending by goods-specific demographic prices based on city-level goods-specific CPIs, and goods-specific spending shares for high, middle, and low-income households.

Similar K-Shaped Retail Spending Pattern in the Second District and in the Nation

National nominal cumulative growth (indexed to 2023)

Percent change

Regional nominal cumulative growth (indexed to 2023)

Percent change

National real cumulative growth (January 2023 = 100%)

Percent change

Regional real cumulative growth (January 2023 = 100%)

Percent change

Sources: Numerator Consumer Spending Data, Consumer Price Index from the Bureau of Labor Statistics via Haver Analytics, and authors’ calculations. Regional charts use three-month moving averages. Notes: Real spending uses corresponding demographic retail prices. Income denotes annual household income.

The above chart shows nominal and real retail spending ex auto from the EHIs at the national level and for the Second District for high (earning $125,000+ a year), middle ($40,000-$125,000) and low-income (less than $40,000) households, in gold, red, and blue respectively. The high-income households represent approximately one third of all households. Retail spending ex auto in the nation includes nonstore (online) purchases while retail spending ex auto in the Second District excludes nonstore purchases to match the analogous concept in MARTS. Both nominal and real retail spending growth in the Second District show a K-shaped pattern that is very similar to the national trend. In every month, cumulative spending growth since 2023 for high-income households exceeds that for middle-income households, while in almost every month, cumulative spending growth for middle-income households exceeds cumulative spending growth for low-income households.

By April 2026, real retail ex auto ex nonstore spending has grown by 4.7 percent relative to January 2023 for the high-income households in the region, but only by 1.8 percent for the middle-income households and has actually shrunk by 0.6 percent for the low-income households. The difference in real spending growth rates between high and low-income groups in the region is almost the same as it is in the nation.

Nominal Gas Spending Decreased in the Nation but Increased in the Region until February 2026

National nominal cumulative growth (indexed to 2023)

Percent change

Regional nominal cumulative growth (indexed to 2023)

Percent change

National real cumulative growth (January 2023 = 100%)

Percent change

Regional real cumulative growth (January 2023 = 100%)

Percent change

Sources: Numerator Consumer Spending Data, Consumer Price Index from the Bureau of Labor Statistics via Haver Analytics, and authors’ calculations. Regional charts use three-month moving averages. Notes: Real spending uses corresponding demographic gas prices. Income denotes annual household income.

We now turn to trends in gasoline consumption in the nation and in the region. The above chart shows nominal and real gas station spending in both the nation and the region for high-, middle-, and low-income households. As we are looking at spending in physical gas stations, the exclusion of nonstore spending in the regional data is no longer an issue and the two sets of series are directly comparable. We see that up until February 2026, the gas spending trends in the nation and in the region have been different—nominal gas spending in the region had approximately held steady and real spending, on average, increased by about 10 percent of the January 2023 level, while nominal gas spending in the nation, on average, had actually declined by 10 percent, and real spending had increased by 5 percent.

K-Shaped Dynamics of Real Gas Consumption Even More Pronounced in Region

National real cumulative growth (February 2026 = 100%)

Percent change

Regional real cumulative growth (February 2026 = 100%)

Percent change

Sources: Numerator Consumer Spending Data, Consumer Price Index from the Bureau of Labor Statistics via Haver Analytics, and authors’ calculations. Notes: Real spending uses corresponding demographic gas prices. Income denotes annual household income.

We now zoom into the last three months of the data to look at real gas consumption trends by income group following the March 2026 gas price shock. To do this, in the chart above, we present the last three months of the data, indexing each series to 100 in February 2026 to better see how real gas consumption by income group differentially evolved relative to the month before gas prices rose. We see that a similar K-shaped pattern opened up in the region and in the nation. High-income households in the region barely decreased real gas spending (0.5 percent between February and April 2026), while low-income households decreased their gas spending by 9.4 percent, with middle-income households in between. In contrast, low-income households in the nation decreased real gas spending by only 3.2 percent, while high-income households marginally increased real gas spending (by 0.4 percent).

It is notable that the K-shaped pattern is actually even more extreme in the region than it is in the nation, a nearly 9 percentage point difference in real spending changes between high- and low-income households in the region, when such differences in the nation are closer to 4 percentage points. The extreme K-shaped dynamics in the Second District may partially be explained by the greater presence of public transportation, enabling commuters to more easily substitute between driving and taking public transit to work.

Looking Ahead

Having taken a regional view of consumer spending, we conclude that the Second District shares many of the same economic trends that have been affecting consumption in the nation, but with its own unique twist. While K-shaped dynamics have been very similar in the nation and the region over the past three years, the region’s gasoline consumption trends following the March 2026 gas price shock have seen an even greater bifurcation between high- and low-income households, with larger reductions in real gas consumption by lower-income groups. This may be a result of the greater development of public transportation in the Second District. We will continue to monitor how consumer spending evolves for different segments of our society both in the region and in the nation in subsequent releases of the EHIs.

Rajashri Chakrabarti is an economic research advisor in the Federal Reserve Bank of New York’s Research and Statistics Group.

Thu Pham is a research analyst in the Federal Reserve Bank of New York’s Research and Statistics Group.

Beck Pierce is a research analyst in the Federal Reserve Bank of New York’s Research and Statistics Group.

Maxim L. Pinkovskiy is an economic research advisor in the Federal Reserve Bank of New York’s Research and Statistics Group.

How to cite this post:

Rajashri Chakrabarti, Thu Pham, Beck Pierce, and Maxim L. Pinkovskiy, "The Regional Side of the Story: K‑Shaped Pattern in Region, Wider Gap in Gas Spending," Federal Reserve Bank of New York Liberty Street Economics, May 28, 2026, https://doi.org/10.59576/lse.20260528BibTeX: View |

@article{ChakrabartiPhamPiercePinkovskiy2026,

author={Chakrabarti, Rajashri and Pham, Thu and Pierce, Beck and Pinkovskiy, Maxim L.},

title={The Regional Side of the Story: K‑Shaped Pattern in Region, Wider Gap in Gas Spending},

journal={Liberty Street Economics},

note={Liberty Street Economics Blog},

number={May 28},

year={2026},

url={https://doi.org/10.59576/lse.20260528}

}

Disclaimer The views expressed in this post are those of the author(s) and do not necessarily reflect the position of the Federal Reserve Bank of New York or the Federal Reserve System. Any errors or omissions are the responsibility of the author(s).

]]>0<![CDATA[Food Insecurity and Consumer Pessimism]]>https://libertystreeteconomics.newyorkfed.org/?p=427152026-05-27T15:39:47Z2026-05-27T14:30:00Zour 2020 analysis of disproportionate financial hardship experienced during the early pandemic and to investigate recent changes in food insecurity and broader economic strains. We then examine how food insecurity relates to the increase in consumer pessimism. We find a remarkable increase in food insecurity, particularly among lower-educated and lower-income households and households with young children. We document a contemporaneous increase in pessimism among the same groups, along with a sharp decline in job-finding expectations. ]]>

Gizem Kosar, Ishva Mehta, and Wilbert van der Klaauw

Current discussions regarding a bifurcated U.S. economy highlight the increasing economic divide between lower- and higher-income Americans in spending and earnings growth and wealth accumulation. While many households are doing fine and economic activity overall has been expanding at a solid pace, large segments of the population are facing high levels of economic insecurity and financial strain, and consumer sentiment on the whole has dropped to low levels. In this post, we use newly collected data from the Survey of Consumer Expectations (SCE) to update our 2020 analysis of disproportionate financial hardship experienced during the early pandemic and to investigate recent changes in food insecurity and broader economic strains. We then examine how food insecurity relates to the increase in consumer pessimism. We find a remarkable increase in food insecurity, particularly among lower-educated and lower-income households and households with young children. We document a contemporaneous increase in pessimism among the same groups, along with a sharp decline in job-finding expectations.

Declining Consumer Sentiment in a K-Shaped Economy

Despite solid economic fundamentals (low unemployment, historically high household net wealth, and resilient consumer spending), consumers overall have been pessimistic about their own financial circumstances and outlook. Current levels of consumer sentiment, capturing how optimistic consumers are about their personal finances and the overall economy, have fallen near or below the low levels seen during the Great Recession and pandemic.

These macroeconomic indicators mask significant heterogeneity across households, supporting the notion of a “K-shaped” economy, in which consumption growth in recent years has been driven largely by higher-income and college-educated households while lower-income households have seen fewer gains. The top of the K-shape reflects high and growing levels of net wealth, fueled by rising stock prices, near-peak home equity levels, and reductions in mortgage payments following the 2020-21 refinance boom. The bottom of the K-shape represents a significant share of the middle- and lower-income population experiencing elevated levels of economic uncertainty and financial hardship. Such financial stress is reflected in concerns about affordability due to the high cost of living, persistent inflation, and high interest rates, and in high delinquency rates for credit cards and auto and student loans.

Lower- and middle-income households generally have experienced higher effective inflation rates, with a greater share of their spending allocated to goods that have seen prices soar since the pandemic, such as housing, groceries, and utilities, causing them to cut back on groceries. The greater financial strain due to the high cost of living, combined with the expiration of pandemic-era aid (such as expanded SNAP benefits), have led to renewed concerns about food insecurity among those at the bottom of the K-shape.

New Evidence from the Survey of Consumer Expectations

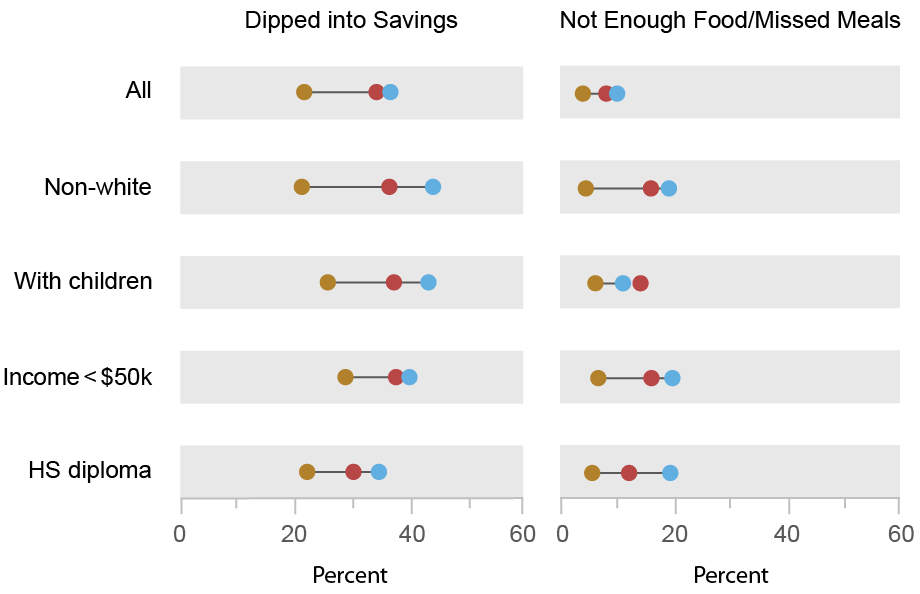

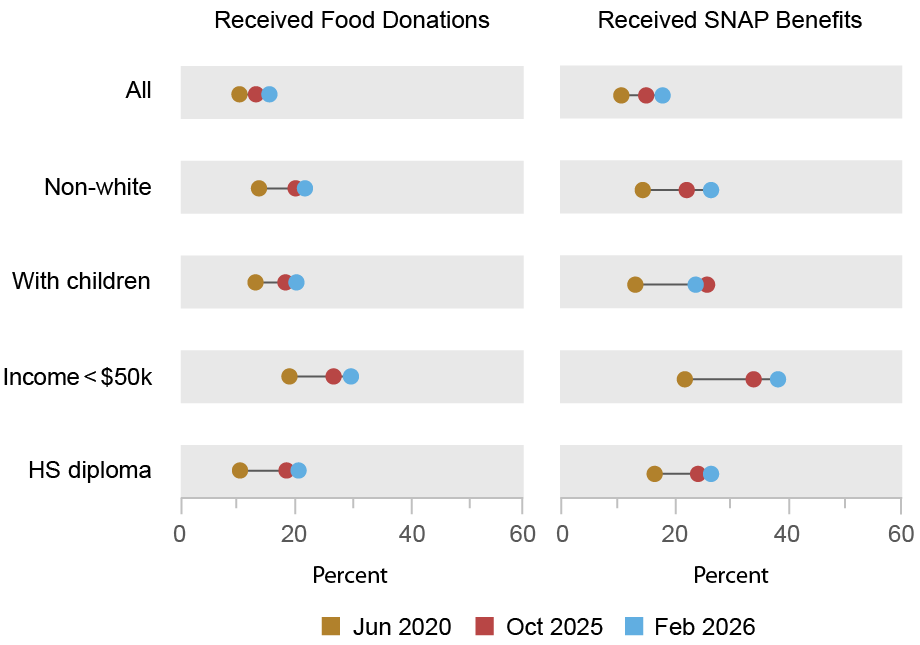

To provide further recent evidence on financial and food insecurity, we draw on the SCE. The SCE is a monthly internet-based survey that has been conducted by the Federal Reserve Bank of New York since June 2013. It is based on a twelve-month rotating panel of roughly 1,200 nationally representative U.S. household heads. As part of its May and June 2020, October 2025, and February 2026 surveys, the SCE included a set of targeted questions to study household financial stress and food insufficiency, as well as households’ expectations about their financial situation a year from now.

Specifically, we asked household heads whether they (or someone in their household) experienced any of the following four events over the prior three months: dipped into savings or emergency accounts to cover expenses; had trouble finding enough food to eat or had kids who missed meals; received food donations from family, friends, or food banks; or received aid through SNAP. Note that eligibility for SNAP benefits is based on household income and size, and is an imperfect proxy for food insecurity. In our analysis, we pool data from the two 2020 surveys and refer to it as the June 2020 survey.

As shown in the charts below, since May/June 2020, and also between October 2025 and February 2026, there have been meaningful increases in the shares of households reporting that they’d experienced the four situations described above. The increases were mostly broad-based across race, age, income, and education groups, but were generally larger for non-whites, lower-income and lower-educated households, and households with children, as detailed in the chart.

Broad-Based Increases in Food Insecurity and Broader Economic Strains Since 2020

Source: Survey of Consumer Expectations, May and June 2020, October 2025, and February 2026 surveys. Notes: The chart shows the shares of respondents in the four surveys (May 2020 and June 2020 results are grouped as June 2020) who reported that over the previous three months they (or someone in their household) had dipped into savings and emergency accounts to cover expenses; had trouble finding enough food to eat or had kids who missed meals; received food donations from family, friends, or food banks; or received aid through SNAP.

While related, our measures differ from the U.S. Department of Agriculture’s (USDA) official survey measure of food insecurity, which aims to capture “the limited or uncertain availability of nutritionally adequate and safe foods, or limited or uncertain ability to acquire acceptable foods in socially acceptable ways.” The USDA’s measure of food insecurity for 2024, its most recent survey, stood at 13.7 percent of households (18.4 percent among households with children). The rate is the highest since reaching a post-2001 low of 10.2 percent in 2021 but remains below its post-2001 high of 14.9 percent attained in 2011. Food insecurity is associated with poor health outcomes as well as lower educational attainment, worker productivity, and lifetime earnings.

Increased Food Insecurity Is Also Associated with Declining Consumer Sentiment

In addition to the increasing trend in these shares, we find that among those reporting incidents of food insufficiency (not enough food, received food donations) and SNAP receipt, there is a lower, and more rapidly declining, net share of respondents expecting to be better versus worse off financially a year from now (as shown in the table below). This means that an increase in the incidence of food insecurity is associated with a deterioration in consumer sentiment. However, the increase in food insecurity clearly is not the only factor that matters—even among those not reporting these incidents of food insecurity we find a sizable decline between 2020 and October 2025 in the net share of respondents expecting to be better versus worse off a year from now, though this decline was followed by partial reversal from October 2025 to February 2026.

Food Insecure Households Report Greater Pessimism on the Economy, Labor Market, and Debt

Household expectations

May/June 2020

October 2025

February 2026

Net share better/worse off

8.0

-4.2

–0.6

– Not enough food/skipped meals

-10.2

-22.1

-32.5

– Received food donations

0.8

-14.8

-22.7

– Received SNAP benefits

0.4

-0.2

-11.7

Average job-finding probability, if were to lose job

48.0

46.8

44.0

– Not enough food/skipped meals

48.8

37.2

41.4

– Received food donations

48.6

37.0

39.4

– Received SNAP benefits

50.1

36.7

33.7

Average debt delinquency probability

11.2

13.1

11.6

– Not enough food/skipped meals

41.4

41.8

32.3

– Received food donations

23.4

30.1

23.4

– Received SNAP benefits

19.6

31.1

20.3

Source: Survey of Consumer Expectations, May and June 2020, October 2025, and February 2026 surveys. Notes: The top panel of the table shows the net share of respondents expecting their household to be financially better versus worse off twelve months from now, overall and for those reporting food need and assistance, in the May/June 2020, October 2025, and February 2026 surveys. The middle panel shows, for each subgroup and survey wave, the average reported percentage chance of finding a job within the following three months, if one’s job were to be lost today. The bottom panel shows the average reported probability of, over the next three months, not being able to make a minimum debt payment. See the SCE questionnaire for the exact question wordings.

Interestingly, we also find considerably larger reductions in the expected job-finding rate (measured as the probability of finding a job in the next three months if one’s current job is lost) for those reporting food needs or SNAP receipt. In contrast, we see little movement over the period in debt delinquency expectations, which measures the probability of missing a minimum debt payment within the next three months—although it’s worth noting that respondents who experience food insecurity have significantly higher debt delinquency expectations. Overall, these trends point to a deterioration in sentiment or an increased pessimism among those who report food insecurity and SNAP receipt.

While not necessarily causal, the observed positive association between food insecurity and overall consumer pessimism, together with the increase in the incidence of food insecurity, especially among households at the bottom of the K-shape, point to a potential explanation for the unusually low recent levels of consumer sentiment at a time when the hard economic data paint a more positive picture.

Gizem Kosar is an economic research advisor in the Federal Reserve Bank of New York’s Research and Statistics Group.

Ishva Mehta is a research analyst in the Federal Reserve Bank of New York’s Research and Statistics Group.

Wilbert van der Klaauw is an economic research advisor in the Federal Reserve Bank of New York’s Research and Statistics Group.

How to cite this post:

Gizem Kosar, Ishva Mehta, and Wilbert van der Klaauw, “Food Insecurity and Consumer Pessimism,” Federal Reserve Bank of New York Liberty Street Economics, May 27, 2026, https://doi.org/10.59576/lse.20260527BibTeX: View |

@article{KosarMehtavanderKlaauw2026,

author={Kosar, Gizem and Mehta, Ishva and van der Klaauw, Wilbert},

title={Food Insecurity and Consumer Pessimism},

journal={Liberty Street Economics},

note={Liberty Street Economics Blog},

number={May 27},

year={2026},

url={https://doi.org/10.59576/lse.20260527}

}

Disclaimer The views expressed in this post are those of the author(s) and do not necessarily reflect the position of the Federal Reserve Bank of New York or the Federal Reserve System. Any errors or omissions are the responsibility of the author(s).

]]>0<![CDATA[Assessing the Current State of Wage Inflation]]>https://libertystreeteconomics.newyorkfed.org/?p=427042026-05-22T17:45:40Z2026-05-26T11:00:00Z]]>

Martin Almuzara, Richard Audoly, and Davide Melcangi

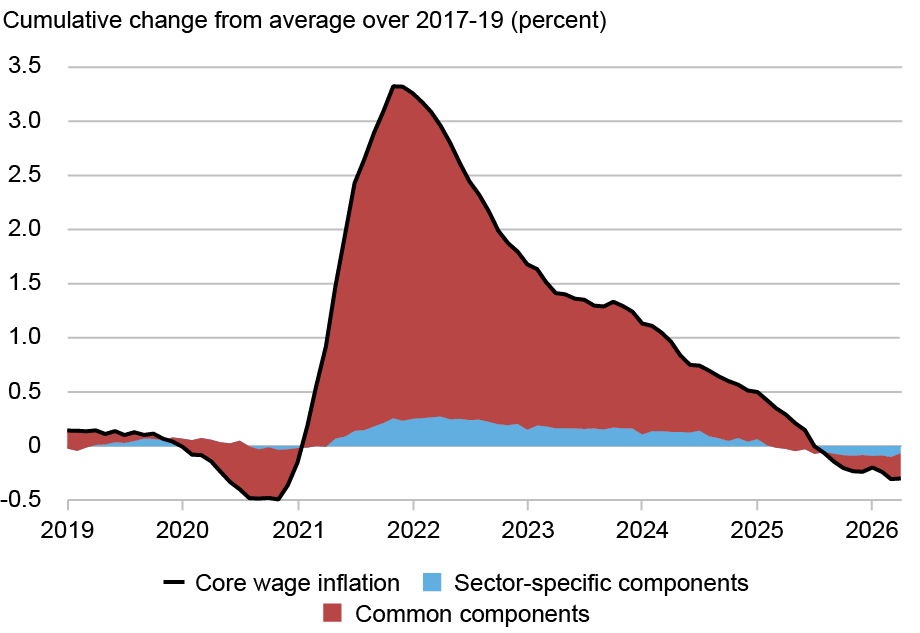

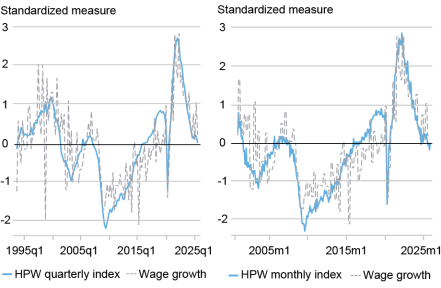

Economists often look at nominal wage growth to gauge labor market imbalances, price pressures, and households’ spending ability. But to use wage growth for these purposes, it is important to look through short-run fluctuations and retrieve underlying wage inflation. In this post, we use our own measure of wage growth persistence—called Trend Wage Inflation (TWIn in short)—to summarize what we learned from wage growth behavior in the past years and draw conclusions for what may lie ahead. Since peaking in late 2021, TWIn has been on a steady decline, reaching levels near those of the 2017-19 period. In the past few months, however, this decline seems to have lost momentum. Our analysis shows that most of the decline in TWIn between 2022 and 2025 was common across industries. Recently, however, a few sectors have shown a decoupling of wage growth dynamics.

Measuring Trend Wage Inflation

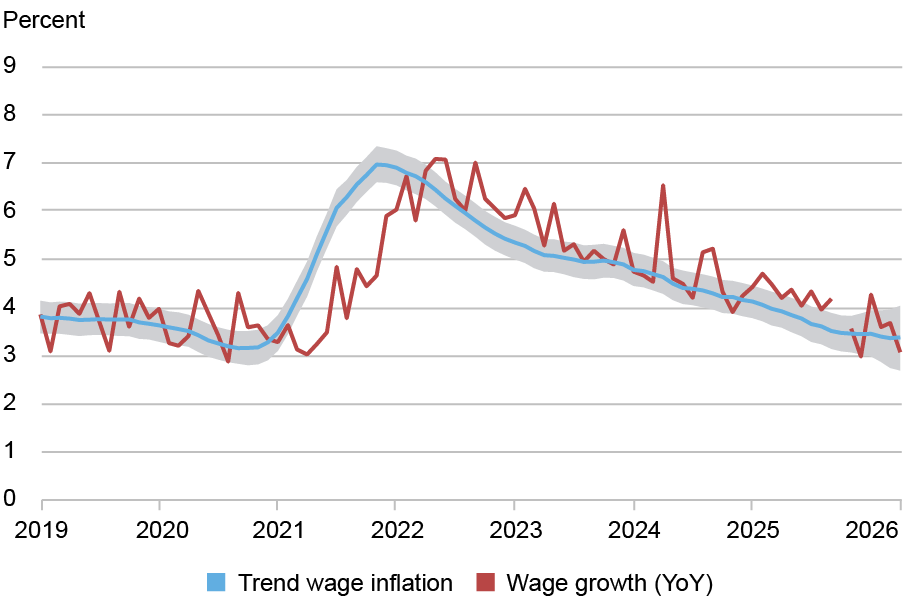

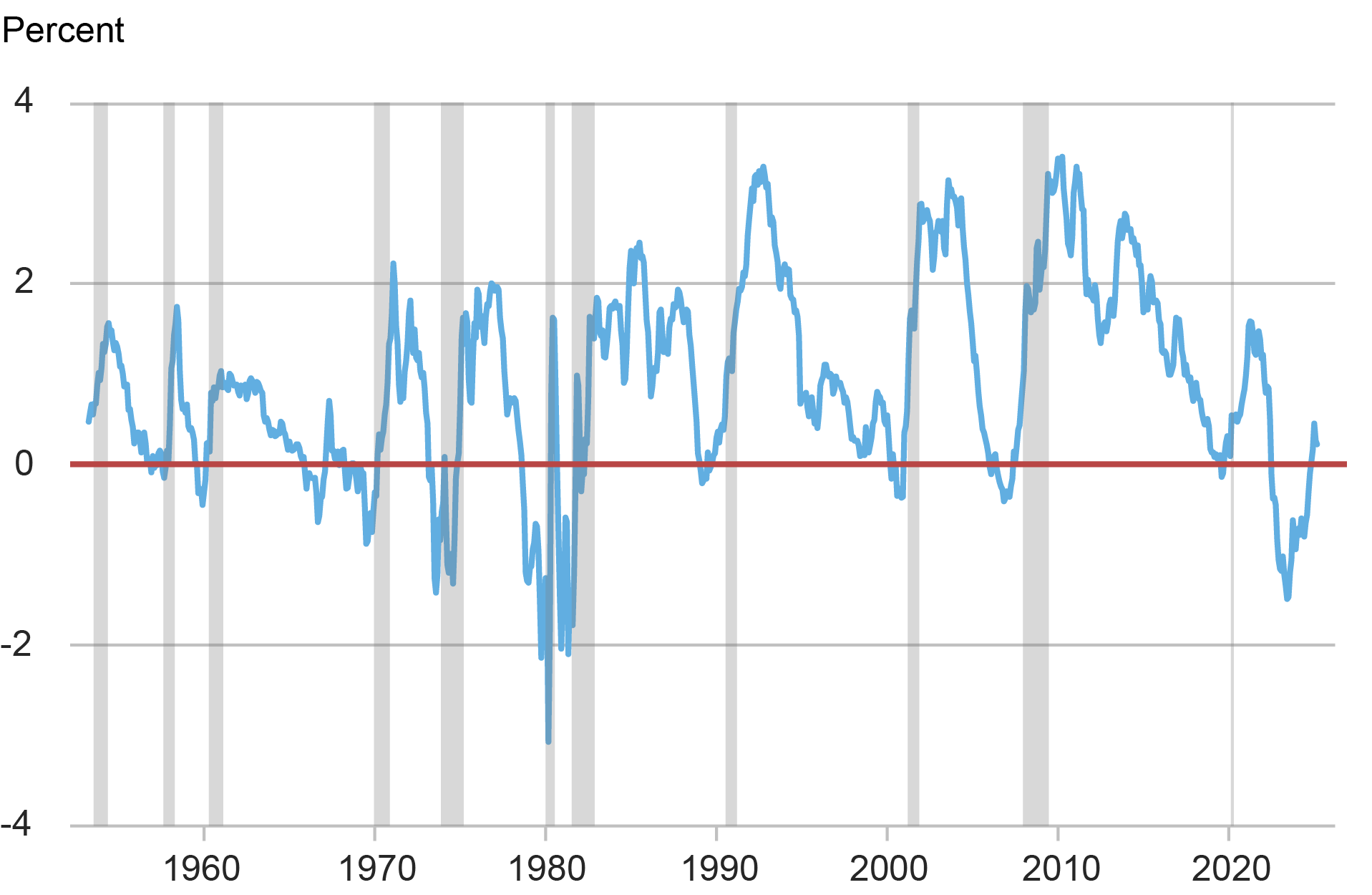

To recover the persistent (“trend”) component of wage inflation, we rely on a framework that combines worker-level data with time series filtering techniques. We have described the methodology in previousposts and in this paper. We estimate a model that decomposes wage growth in each industry into a persistent component and a noise term capturing transitory variation and measurement error. Each component is further split into a common and an industry-specific term. The chart below shows our estimated trend (TWIn, blue line), together with the realized twelve-month wage growth (red line). The shaded area around the trend is a 68 percent confidence band that captures the uncertainty associated with the estimates.

Trend Wage Inflation May Have Steadied After a Prolonged Period of Moderation

Sources: Bureau of Labor Statistics; Current Population Survey; authors’ estimates. Note: The gap in the wage growth line reflects the absence of October 2025 wage data due to the U.S. government shutdown.

Since its peak toward the end of 2021, TWIn has been steadily declining, with the exception of the second half of 2023: that plateau, which we discussed in an earlier post, turned out to be transient. Looking closer at the recent months, TWIn appears to have leveled off again, this time near the 2017-19 average. This recent flattening is consistent with other signs of labor market stabilization. The unemployment rate has changed little since the end of last summer. And the HPW Labor Market Tightness Index, despite some ups and downs, has hovered near zero for several months, a value reflecting broadly balanced labor market conditions. This behavior therefore confirms our earlier analysis that TWIn moves in tandem with measures of labor market tightness.

Note that compared to the second half of the 2010s, the gap between TWIn and measures of trend price inflation, like the Multivariate Core Trend (MCT) inflation, is narrower, suggesting that households’ earnings have been growing more slowly in real terms.

Looking Under the Hood of Trend Wage Dynamics

Our methodology also allows us to investigate whether specific industries have disproportionately contributed to the dynamics of trend wage inflation. As a first step, in the chart below, we decompose the cumulative change in TWIn since its 2017-19 average into changes that are common across industries and changes that are industry-specific. The decline in TWIn since its peak was widespread across the economy. In other words, the common force that pushed up wage inflation in 2021 subsided thereafter.

Most of the TWIn Dynamics Have Been Common Across Industries

Sources: Bureau of Labor Statistics; Current Population Survey; authors’ estimates.

While quantitatively less sizable, sector-specific components of trend wage inflation have also retracted. As we discuss in the paper, these components typically tend to capture lower-frequency movements in trend wage inflation. In some instances, however, they can signal that trend wage dynamics in an industry are decoupling from the rest of the economy.

In this context, our analysis highlights two industries worth discussing. First, wage inflation of public administration workers has followed delayed dynamics with respect to the rest of the economy. This is not surprising: our analysis over a long time period shows that this industry always displays a strong idiosyncratic component.

Another industry in which wage inflation has remained higher than the rest of the economy is construction and mining. Our analysis suggests that these dynamics may be idiosyncratic to that industry, rather than a reflection of different sensitivities to a common factor. In the chart below, we show trend wage inflation in construction and mining (in red), in public administration (in gold), and in the aggregate (in blue).

Most but Not All Industries Have Seen a Synchronized Decline in Wage Growth

Trend wage inflation (percent)

Sources: Bureau of Labor Statistics; Current Population Survey; authors’ estimates.

The idiosyncratic trend specific to the construction and mining industry has risen since 2022, in contrast with economy-wide downward pressures to wage growth. As a result, wage growth in this industry has been consistently and persistently stronger than in the rest of the economy. This pattern could be related to construction of AI data centers, with sustained labor demand fueling wage inflation. Recent reductions in net immigration could work in the same direction, especially since the construction industry tends to rely on immigrant workers.

In summary, our measure of persistent nominal wage growth, TWIn, provides an indication of underlying wage inflation. After a prolonged period of moderation, the easing in our TWIn measure appears to have slowed. This stabilization, at levels near those seen in the second half of the 2010s, is consistent with a broadly balanced labor market. Looking ahead, considerable uncertainty remains. On the one hand, specific industries such as construction may continue to put some upward pressure on wage inflation, as they have done in recent months. On the other hand, any deterioration of labor market conditions could result in renewed downward pressure on wage inflation.

Martín Almuzara is a research economist in the Federal Reserve Bank of New York’s Research and Statistics Group.

Richard Audoly is a research economist in the Federal Reserve Bank of New York’s Research and Statistics Group.

Davide Melcangi is an economic research advisor in the Federal Reserve Bank of New York’s Research and Statistics Group.

How to cite this post:

Martin Almuzara, Richard Audoly, and Davide Melcangi, “Assessing the Current State of Wage Inflation,” Federal Reserve Bank of New York Liberty Street Economics, May 26, 2026, https://doi.org/10.59576/lse.20260526BibTeX: View |

@article{AlmuzaraAudolyMelcangi2026,

author={Almuzara, Martin and Audoly, Richard and Melcangi, Davide},

title={Assessing the Current State of Wage Inflation},

journal={Liberty Street Economics},

note={Liberty Street Economics Blog},

number={May 26},

year={2026},

url={https://doi.org/10.59576/lse.20260526}

}

Disclaimer The views expressed in this post are those of the author(s) and do not necessarily reflect the position of the Federal Reserve Bank of New York or the Federal Reserve System. Any errors or omissions are the responsibility of the author(s).

]]>1<![CDATA[AI’s Macroeconomic Challenges and Promises]]>https://libertystreeteconomics.newyorkfed.org/?p=422772026-06-02T15:12:45Z2026-05-20T11:00:00Z

Simone Lenzu

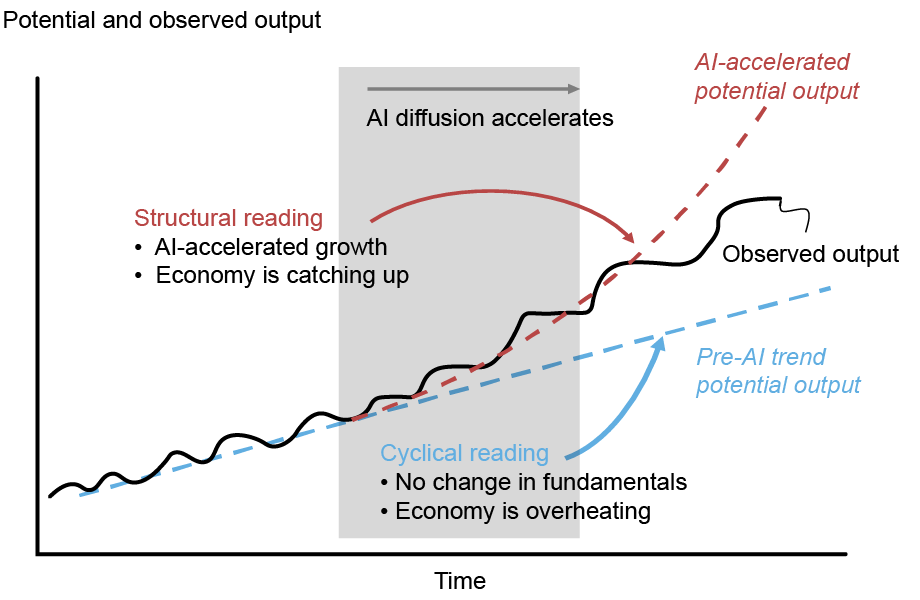

In the third quarter of 2025, America’s largest tech firms for the first time spent more on capital investment than they earned from operations. The implication is that AI, a technology with the potential to make the economy more productive, is, for now, absorbing resources faster than it is generating returns. This post discusses how the tension between AI’s long-run promise and its short-run costs affects the outlooks for inflation, real activity, and financial stability.

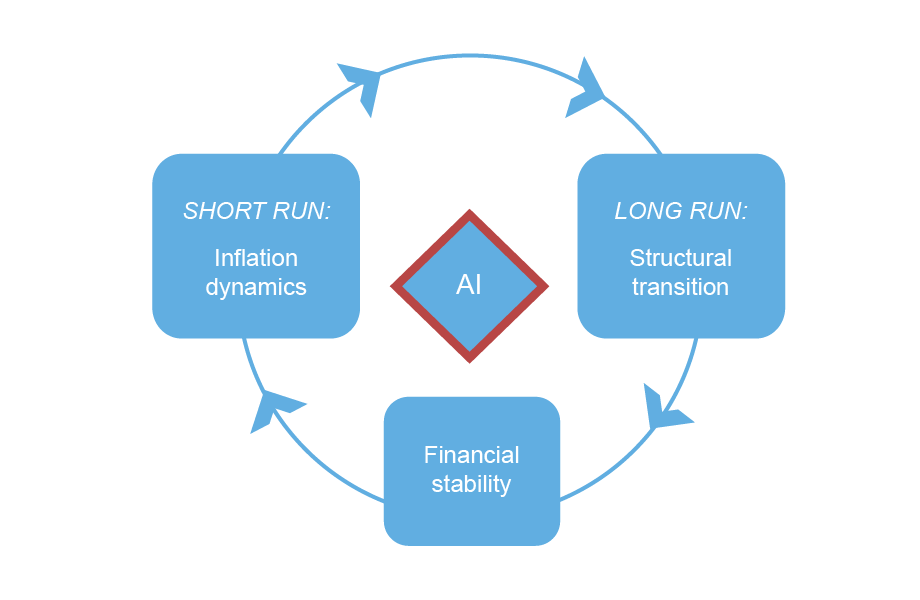

Three Channels, One Framework

Drawing on my research, I describe three interrelated channels—inflation dynamics, structural transition, and financial stability—through which AI bears on the economy (see figure below).

Three Channels Through Which Diffusion of AI Can Affect the Economy

Source: Author’s illustration.

Inflation Dynamics

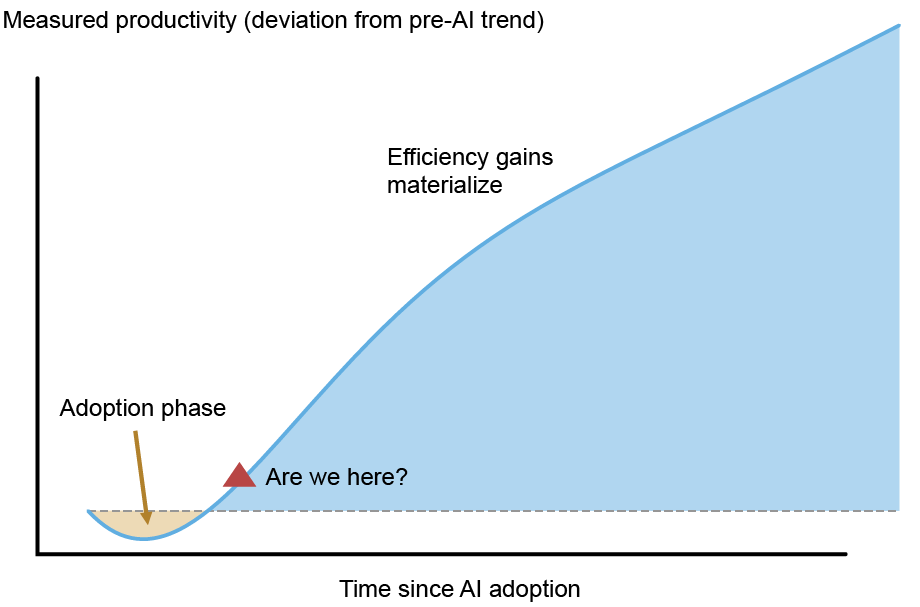

In the short run, the diffusion of AI can reshape how interest rates influence inflation and real activity. A widely held view is that AI, by raising productivity, will be a powerful disinflationary force. This view may ultimately prove correct, but it skips a crucial step. What matters for inflation is not whether AI raises productivity, but whether it raises productivity faster than it increases the costs of adopting it.

During the transition, firms divert substantial resources toward reorganization, data infrastructure, and integration, which can temporarily raise production costs even as the technological frontier expands. This is the so-called “productivity J-curve,” depicted in the figure below.

Measured Productivity Can Fall During the Adoption Phase

Source: Stylized illustration based on Brynjolfsson, Rock, and Syverson (2021).

The effects on prices, on the other hand, are already visible in input markets. In 2025, the major AI firms (Google, OpenAI, Anthropic, Meta, Amazon, Oracle) committed roughly $300 billion to capital investment across semiconductor supply chains, power grids, and specialized labor. Aggressive investment spending continued into the first quarter of 2026 and is projected to rise further, adding to cost pressures across the economy.